FireEye was right about almost everything that mattered in cybersecurity and still managed to lose. Between 2004 and 2021, a company founded by a Pakistani-American engineer named Ashar Aziz invented the modern category of advanced threat detection, named the adversaries that now dominate every board-level security conversation, took the world's premier incident response firm under its roof, caught the most significant nation-state breach of the decade, and then disassembled itself into pieces that two different buyers carried away. According to SEC filings, the products business that Aziz built sold to Symphony Technology Group in October 2021 for $1.2 billion in cash, while the consulting and intelligence operation that Kevin Mandia ran sold to Google for $5.4 billion in cash. in September 2022. The sum of those parts, roughly $6.6 billion gross, is less than CrowdStrike's market capitalization adds in a typical good trading week in 2026. According to multiple market data sources, CrowdStrike's market value sat between $128 billion and $151 billion in May 2026, more than twenty times what FireEye plus Mandiant ultimately fetched on the block.

That gap is the case study. FireEye saw zero-day attacks before signature-based antivirus vendors would admit such things existed. Mandiant named the Chinese People's Liberation Army cyber units that were already inside the Fortune 500. Both companies were technically vindicated almost beyond dispute. The question this article works through is why a company can be early, correct, technically excellent, and admired by its peers, and still cede the prize to a competitor founded seven years later by a former McAfee executive who chose a different delivery model. The answer matters for any founder building category-defining technology, any board approving a major acquisition, and any product leader weighing on-premises revenue against a SaaS migration that will cannibalize it.

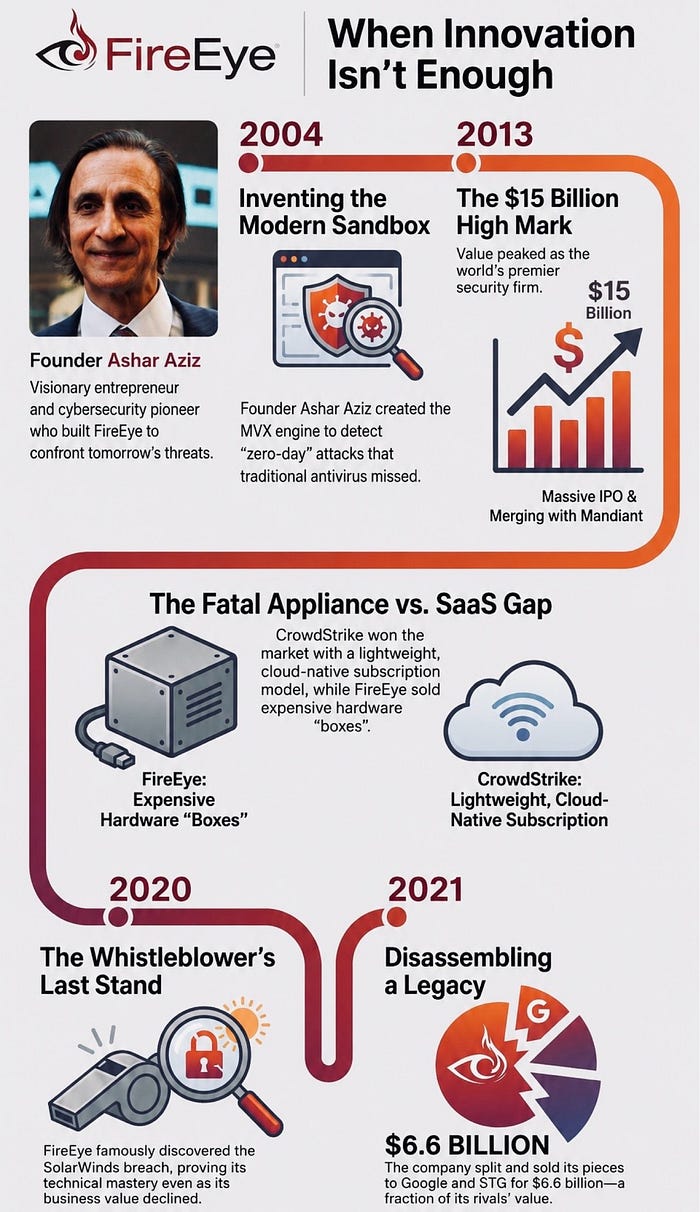

The Founder Who Saw Zero-Days Before the Market Did

According to PitchBook records and his MIT Electrical Engineering and Computer Science department profile, Ashar Aziz was born in Karachi in 1959. and spent his early academic years at Middle East Technical University in Ankara before transferring to MIT, where he earned an S.B. in electrical engineering and computer science in 1981. He went on to complete an M.S. in computer science at the University of California, Berkeley on a U.C. Regents Fellowship. According to a SkyElectric biography and his FireEye S-1 filing, Aziz spent twelve years at Sun Microsystems as a Distinguished Engineer. working on networking and network security, and eventually served as chief technology officer of Sun's N1 utility computing program until October 2003. Along the way he founded a data center automation company called Terraspring in June 1999. According to PitchBook, Sun acquired Terraspring in November 2002. in the depths of the dot-com hangover, and Aziz folded the technology into Sun's broader virtualization roadmap.

The genesis of FireEye lay in the moment Aziz left Sun. According to the FireEye S-1 registration statement filed with the Securities and Exchange Commission in August 2013, the company was incorporated in Delaware in February 2004 under the name NetForts, Inc. and changed its name to FireEye, Inc. in September 2005. Its headquarters were in Milpitas, California, the unglamorous industrial spine of Silicon Valley along Interstate 880. In a candid quote later carried by Hayat Life magazine, Aziz described the founding years in unsparing terms: "Back in 2008, things were bleak. We didn't have any paying customers, couldn't raise money and we were running out of cash. Most of my executive team and half of the engineers quit." According to his Wikipedia entry and the MIT EECS profile, he worked from home for the first stretch, putting in eighty to one hundred hour weeks and seeding the business with roughly $4,000 from his own savings.

What Aziz built was conceptually clean and commercially radical. Traditional antivirus and intrusion detection relied on signatures, fingerprints of known malware compared against incoming files. According to the S-1, FireEye instead engineered what it called the Multi-Vector Virtual Execution engine, or MVX, which detonated suspicious files, web sessions, and email attachments inside isolated virtual machines and watched what they did. If a file tried to inject code into another process, contact a command-and-control server, or modify the registry in suspect ways, FireEye flagged it regardless of whether anyone had ever seen that exact piece of malware before. The FireEye S-1 put it this way: "We have invented a purpose-built, virtual machine-based security platform" whose MVX engine "identifies and protects against known and unknown threats that existing signature-based technologies are unable to detect."

This was the first commercially scaled answer to what the security profession had begun to call advanced persistent threats. According to multiple sources including the TaoSecurity blog and Wikipedia entries on the term, "advanced persistent threat" was coined inside the U.S. Air Force around 2006 or 2007, credited to Colonel Greg Rattray, as an unclassified label that let cleared personnel discuss classified intrusion sets in mixed company. Mandiant would later popularize the phrase, but the underlying problem, that nation-state attackers wrote bespoke malware for specific targets and burned signature-based defenses on first encounter, was already a quiet emergency in 2008 and 2009. FireEye's sandbox approach was the right answer to that problem at the right time.

The capital followed. According to FireEye's own corporate blog and SEC filings, the company's venture syndicate included Sequoia Capital. led by Doug Leone with help from Gaurav Garg, Norwest Venture Partners, JAFCO Ventures, DAG Ventures, Juniper Networks as a strategic investor, Four Rivers Partners, Goldman Sachs, and Silicon Valley Bank. In November 2009, according to a FireEye press release reported by VentureBeat, In-Q-Tel, the venture arm of the U.S. intelligence community, joined the cap table, an endorsement that opened doors at federal agencies. By the end of January 2013, according to Reuters and VentureBeat, FireEye had raised roughly $100 million in total private capital, with the final pre-IPO round of $50 million coming from Sequoia, Norwest, Goldman, Juniper, and SVB.

The post-Stuxnet years were the perfect tailwind. Stuxnet, the worm that damaged Iranian centrifuges and surfaced publicly in 2010, made nation-state cyber operations a boardroom topic. Aurora, the 2009 Chinese campaign against Google and a long list of other U.S. companies, did the same. Aziz had built the right product for executives who had just learned that their existing security stack was theatre. FireEye's appliances landed in financial institutions, defense contractors, and federal agencies that were actively being breached and were willing to pay six and seven-figure sums for a box that could see what their incumbent vendors could not.

Dave DeWalt Arrives and Wall Street Falls in Love

By 2012 the company had a product, a customer base, and a problem common to deeply technical founders. According to a Forbes profile referenced in later interviews, the magazine had already labeled FireEye "Silicon Valley's hottest security start-up" in 2012, and Aziz's team had grown well beyond the size at which an inventor-CEO can easily run things alone. The board's answer was to recruit David DeWalt. According to a FireEye executive biography filed with the SEC and corroborated by BankInfoSecurity, DeWalt joined as chairman in mid-2012 and was named chief executive officer in November 2012. He brought a specific kind of credibility. He had served as president and CEO of McAfee from April 2007 until February 2011, and according to multiple press accounts of that era he engineered McAfee's $7.7 billion sale to Intel, then the largest acquisition in Intel's history. Before McAfee he had been chief executive of Documentum, which sold to EMC in 2003. for $1.9 billion.

Aziz stepped into the role of vice chairman, chief technology officer, and chief strategy officer. According to FireEye filings, he retained roughly ten percent of the company. and remained the technical voice, but the day-to-day operating cadence shifted to DeWalt and the team he assembled. DeWalt's strategy was straightforward and, for a window of time, brilliant. He positioned FireEye as the premium platform for catching the threats other vendors missed. The pricing carried that premium. According to filings, FireEye sold a network appliance plus a Dynamic Threat Intelligence. cloud subscription that bundled software, services, and intelligence updates. Gross margins on the product line were comfortably above seventy percent.

The financial trajectory was what venture capitalists dream about. According to the S-1, revenue grew from $11.8 million in 2010 to $33.7 million in 2011, $83.3 million in 2012, and $161.6 million in 2013. Net losses widened as the company spent on sales and marketing, but the top line growth justified the burn. Headcount climbed from roughly 175 in 2011 to about 900 by mid-2013, according to a corporate encyclopedia entry on the company.

The IPO arrived on Friday, September 20, 2013. According to Bloomberg, TechCrunch, and Reuters coverage, FireEye priced 15.2 million shares at $20, well above the initial range of $12 to $14. and the revised range of $15 to $17. The stock opened at $40.30, traded as high as $44.89, and closed at $36, an 80 percent first-day pop. According to TechCrunch, the implied first-day market capitalization was approximately $2.3 billion. on revenue that would finish 2013 at $161.6 million, a multiple of more than fourteen times trailing revenue. Wall Street Journal reporting from the following March pegged the trading multiple at roughly 69 times sales when the stock reached its peak. According to Yahoo Finance historical data and a later BankInfoSecurity interview with DeWalt, the share price topped out around $97. 35 in March 2014, briefly carrying the implied enterprise value to roughly $16 billion.

That moment, March 2014, was the high water mark. Almost everything that followed concerns the slow, expensive process of finding out what FireEye was actually worth.

Mandiant and the Building in Pudong

While Aziz had been building a product company in Milpitas, Kevin Mandia had been building something different on the East Coast. According to his bio in the FireEye 8-K filing announcing the 2013 merger and his Wikipedia entry, Mandia had served as a U.S. Air Force officer, holding a position as a computer security officer and special agent in the Air Force Office of Special Investigations. He went on to run incident response and computer forensics at Foundstone, the security boutique founded by Stuart McClure that McAfee acquired in 2004. According to the TaoSecurity blog of Richard Bejtlich, who joined Mandiant in 2011 as chief security officer, Mandia founded a consulting practice called Red Cliff Consulting LLC in 2004 in Alexandria, Virginia. According to a 2006 press release archived on Forensic Focus, Red Cliff was rebranded as MANDIANT in February 2006 after a year of 150 percent revenue growth.

The Mandiant culture had a distinct character. Its consultants were operator-led, frequently former military or intelligence personnel, and they marketed themselves on the strength of having actually run intrusions out of customer networks. According to a Wikipedia entry on the company corroborated by reporting in CNBC, Kleiner Perkins Caufield and Byers and One Equity Partners, the private investment arm of JPMorgan Chase, invested in Mandiant in 2011. According to the same sources, Mandiant generated more than $100 million in revenue in 2012, up 76 percent from 2011, and reached approximately 500 employees by the time of the FireEye merger. Mandia's team built OpenIOC, the XML-based standard for indicators of compromise, and a product called Mandiant Intelligent Response that allowed investigators to query thousands of endpoints at once during a breach.

What turned Mandiant from a respected consultancy into a globally known brand was the APT1 report, released on February 18, 2013. According to the report itself, titled "APT1: Exposing One of China's Cyber Espionage Units," Mandiant attributed a multi-year cyber espionage campaign against at least 141 organizations. across 20 major industries to the 2nd Bureau of the People's Liberation Army General Staff Department's 3rd Department, also known by its Military Unit Cover Designator 61398. The report named a specific. 130,663 square foot, 12-story building on Datong Road in the Gaoqiaozhen area of Pudong, Shanghai. It published more than 3,000 indicators of compromise, 13 X.509 encryption certificates, and details on more than 40 malware families. It went further and identified three individual personas inside the unit, including "UglyGorilla," whom Mandiant identified as Wang Dong, and "SuperHard," identified as Mei Qiang.

The most-quoted line in the report, taken directly from its executive summary, ran: "Either a secret, resourced organization full of mainland Chinese speakers with direct access to Shanghai-based telecommunications infrastructure is engaged in a multi-year, enterprise-scale computer espionage campaign right outside of Unit 61398's gates, performing tasks similar to Unit 61398's known mission, or APT1 is Unit 61398." China's Foreign Ministry spokesman Hong Lei, according to Xinhua reporting reproduced at the time, called the allegations "groundless" and "irresponsible and unprofessional." The U.S. Department of Justice subsequently indicted five PLA officers in May 2014 in the first such prosecution of state-sponsored economic cyber espionage. Mandiant did not coin the term APT, but APT1 did more than any other document to standardize the vocabulary by which boards, regulators, and security teams talk about nation-state activity.

That brand was what FireEye bought. According to FireEye's SEC Form 8-K filed with a January 2, 2014 announcement and the subsequent Form 424B3 prospectus, the merger had legally closed on December 30, 2013. The aggregate consideration was approximately $989.4 million, consisting of about $106.5 million in net cash and 21.5 million shares and options of FireEye common stock. Most press coverage, including CNBC, rounded the figure to $1.05 billion. based on the share price on the closing date. DeWalt explained the rationale on the announcement call, according to FireEye's Exhibit 99.1: "Mandiant is often the first call that is made when a serious breach has occurred in an organization. Strategically, Mandiant brings us closer to the breach when it occurs, and we believe this is critical to increasing pull for our products, shortening our sales cycle and accelerating our growth." Kevin Mandia, in the same press release, called the combination "fully integrated products and services that help organizations protect themselves from attacks." Mandia joined the combined company as senior vice president and chief operating officer.

The strategic logic looked airtight. FireEye had the technology that detected attacks; Mandiant had the brand that responded to them. Customers in the middle of an active breach would have one phone number to call. Threat intelligence flowing back from incident response engagements would sharpen the MVX engine's detections. Mandiant consultants would arrive on site, deploy FireEye appliances, and convert short consulting engagements into long product subscriptions. The market liked the story. FireEye's stock continued its rally into March 2014 and the combined enterprise value briefly crossed $15 billion.

A Billion-Dollar Marriage of Opposites

The integration did not work the way the deck promised. According to a September 2021 analysis by Forrester analyst Jeff Pollard, "the FireEye and Mandiant cultures never truly meshed. FireEye personnel were masters of hardware sales, while Mandiant cultivated a culture of expertise and mastery." Pollard described a "post-acquisition brain drain leading to a Mandiant diaspora," a phenomenon corroborated in subsequent reporting by TechTarget's Eric Parizo of Omdia, who noted that "the 2014 merger also created some channel conflicts since Mandiant relies heavily on consulting and security services engagements." The strategic analysis publication Strategy of Security captured the underlying tension in plain terms: "it's difficult to grow both a product (FireEye) and a services business (Mandiant) at the same time. Especially when your CEO started the services business."

The mechanical sources of friction were predictable in retrospect. Mandiant's consultants earned utilization-based compensation tied to billable hours; FireEye's sales force lived on quarterly bookings against quota and accelerator schedules tied to multi-year appliance deals. The Mandiant motion was to enter a customer in the middle of a breach, install monitoring, and earn trust over months; the FireEye motion was to land a six-figure box sale on a 90-day sales cycle and renew the threat intelligence subscription. Mandiant viewed themselves as elite operators conducting a craft; FireEye sales reps viewed themselves as enterprise software professionals delivering a number. According to CISO Lens analyst James Turner's LinkedIn commentary later, "the commoditization of intelligence into a product aspect has always been a struggle for FireEye."

The revenue mix told the story. According to FireEye's 10-K filings on EDGAR, total revenue grew from $161.6 million in 2013 to $425.7 million in 2014, an extraordinary 163 percent jump. driven primarily by adding Mandiant's services revenue, and to $623.0 million in 2015. But the composition was changing. Product revenue, the high-margin appliance line, fell from $216.6 million in 2015 to $151.9 million in 2016, while subscription and services revenue grew from $406.3 million to $562.2 million. By 2020, according to the FY2020 10-K, FireEye's professional services line generated $215.6 million, while product, subscription, and support together contributed $724.9 million, growing just 2.2 percent year over year. The Wall Street narrative of a software company with sandbox-driven moat margins was, by 2017, no longer descriptive of the actual business.

DeWalt continued to acquire. According to a FireEye press release and SEC filings, the company purchased nPulse Technologies in May 2014 for approximately $60 million in cash plus stock. subject to milestones; total purchase consideration was later disclosed at $56.6 million. In January 2016, according to a SecurityWeek report and FireEye's announcement, FireEye bought iSIGHT Partners, a threat intelligence firm, for $200 million in cash plus up to $75 million in earnouts, a potential total of $275 million. Days later, according to a FireEye press release, the company purchased Invotas International, a security orchestration startup. with 19 employees. The acquisitions added pieces to a platform vision but did not solve the underlying tension between expensive hardware boxes and a market that was moving to cloud-delivered software.

On May 5, 2016, according to Reuters and a FireEye Form 8-K, the company announced that DeWalt would transition out of the chief executive role effective June 15, 2016, and that Kevin Mandia would replace him. DeWalt remained as executive chairman until February 2017, when he resigned entirely. according to Fortune reporting. On the same announcement call, according to a Reuters account, JPMorgan analyst Sterling Auty asked DeWalt directly whether the company had tried to sell itself and the process had failed; DeWalt did not directly confirm or deny.

Mandia inherited a company that had peaked. According to Reuters reporting on the August 4, 2016 second-quarter call, services revenue growth had slowed from 40 percent the prior quarter to just 2 percent year over year. Mandia's own explanation captured the demand-side problem: "While our services personnel are responding to more attacks this year than prior years, the scope and scale of these attacks is simply different. The average duration and size of each incident response engagement was smaller than in years past. Suddenly, we're doing forensics and deep-diving four machines or five machines." On the same day FireEye announced layoffs of 300 to 400 employees out of roughly 3,400, with the chief financial officer Mike Berry targeting roughly $80 million in annual cost reduction, according to Reuters. The stock fell 16.2 percent in extended trading to $14.02, down nearly 70 percent year over year and roughly 85 percent from the March 2014 peak.

The Cloud-Native Generation Arrives

While FireEye's product business shrank, a different company was scaling. According to multiple corporate histories, CrowdStrike was co-founded in November 2011 by George Kurtz, the former chief technology officer of McAfee who had worked for DeWalt, and Dmitri Alperovitch, the former McAfee vice president of threat research who had publicly attributed the Aurora intrusions to Chinese actors in 2010. The third co-founder, Gregg Marston, served as the initial chief financial officer. CrowdStrike's Falcon platform, according to its corporate timeline and Wikipedia entry, launched in June 2013. The architectural choice was the consequential one. Falcon ran as a single lightweight agent on the endpoint, communicating telemetry to a multi-tenant cloud back end. built on Amazon Web Services. Kurtz described the design publicly as "the Salesforce of security."

The economics were structurally different from FireEye's. FireEye sold a $100,000 to $500,000 appliance plus a recurring subscription. Each box had to be racked, configured, tuned, and refreshed every three to five years. CrowdStrike sold a cloud subscription billed per endpoint per year, with no hardware to ship and no on-premises infrastructure for customers to maintain. According to the Strategy of Security publication, "FireEye wasn't able to maintain its market leadership in the transition from its on-premise hardware and software business to a modern SaaS model. Fast-moving competitors like CrowdStrike and SentinelOne took over the endpoint protection market that FireEye was pivoting towards." Forrester's later verdict was more brutal: FireEye products "never displaced incumbents. Firewalls still exist, and sandbox functionality became a feature of them."

The data moat compounded the structural advantage. Every Falcon endpoint streamed telemetry to a shared cloud back end that CrowdStrike called the Threat Graph. As the installed base grew, the graph saw more attacker behavior, which trained more detection logic, which improved the product, which sold more endpoints. FireEye's appliances, by contrast, lived inside customer networks and sent only sampled metadata back to the Dynamic Threat Intelligence cloud. There was no equivalent network effect. According to a Piper Jaffray reseller survey reported in December 2016, "demand for FireEye has gotten worse and they are no longer leading with FireEye products for advanced threat protection."

CrowdStrike priced its initial public offering on June 11, 2019 at $34 per share, above the marketed range of $28 to $30. According to CNBC and the CrowdStrike press release, the stock opened at $63.50 and closed at $58 on its first trading day, a 70.6 percent pop that valued the company at roughly $11.4 billion at the close, intraday peak of about $12.2 billion. According to CrowdStrike's most recent SEC filings, revenue grew from $249.8 million in fiscal 2019 to $3.06 billion in. fiscal 2024 and $3.95 billion in fiscal 2025, reaching $4.81 billion in fiscal 2026, the year ending January 31, 2026. Ending annual recurring revenue at January 31, 2026 stood at $5.25 billion, up 24 percent year over year. The company's market capitalization in May 2026, according to data from CompaniesMarketCap, Public.com, Robinhood, and Morningstar, ranged from roughly $128 billion to $151 billion depending on the trading day. CrowdStrike's outage on July 19, 2024, when a faulty Falcon sensor content update crashed approximately 8.5 million Windows systems globally, dented the stock roughly 45 percent over the following weeks. and triggered a Delta Air Lines lawsuit seeking around $500. million, according to Wikipedia's compiled account of the incident and CrowdStrike's subsequent 10-Q disclosures, yet by mid-2026 the share price had largely recovered.

The fate of the broader sandbox-era cohort was not kind. Damballa, an Atlanta-based botnet detection startup that had raised significant venture capital, sold to Core Security in July 2016 in what SecurityWeek characterized as a fire sale at roughly $9 million. Cyphort, a sandbox competitor that had taken $53.7 million in venture funding, sold to Juniper Networks in August 2017 at undisclosed terms widely understood to be small. Lastline, a Santa Barbara research-led sandbox vendor, sold to VMware in June 2020 at roughly $110 million net of cash according to S&P Capital IQ data, after which VMware laid off about 40 percent of the Lastline team, according to TechCrunch. Bromium, the Xen-based microvirtualization isolation vendor founded by Simon Crosby and Ian Pratt, sold to HP in September 2019 at undisclosed terms. Cylance, the AI-first endpoint vendor, sold to BlackBerry on February 21, 2019 for $1.4 billion in cash, a deal that BlackBerry's subsequent results suggested was overpriced; BlackBerry sold the Cylance endpoint business to Arctic Wolf in 2024. Bit9/Carbon Black sold to VMware in October 2019 for $2.1 billion enterprise value at $26 per share, according to VMware's SEC filings, and is now inside Broadcom following Broadcom's November 2023 VMware acquisition. Sourcefire, the IDS pioneer that became Cisco's threat detection foundation, sold to Cisco in July 2013 for approximately $2.7 billion, the high water mark for the cohort.

In other words, of roughly a dozen sandbox-era and behavior-based detection vendors that competed in FireEye's segment, none built a durable independent business. The category they pioneered was absorbed into broader platforms. CrowdStrike, SentinelOne, Palo Alto Networks, and Microsoft now serve the workloads those companies were built for. According to Microsoft's January 2023 earnings disclosures cited by Cybersecurity Dive, Microsoft Security revenue crossed $20 billion in calendar 2022, up 33 percent year over year, making Microsoft the largest cybersecurity vendor in the world by revenue. Palo Alto Networks, under Nikesh Arora since June 2018, has grown from roughly $19 billion in market value at his arrival. to roughly $130 to $200 billion through 2025 and 2026, according to multiple market data sources, with Robinhood reporting a $198 billion value in May 2026.

The Phone Call That Broke SolarWinds

For most of 2018, 2019, and 2020, FireEye looked like a company managing decline. Revenue grew from $831.0 million in 2018 to $940.6 million in 2020, but net losses ran $207 to $257 million each year. The Helix security operations platform, launched at the FireEye Cyber Defense Summit in late November 2016. and generally available in. spring 2017, never displaced Splunk in the SIEM market or the major SOAR vendors in the orchestration space. According to Forrester's 2021 retrospective, "FireEye's other offerings such as TAP and Helix never took over the security analytics or security orchestration, automation, and response space."

Then, on December 8, 2020, FireEye announced that it had been breached, and the trajectory of the company changed.

The mechanics of the discovery, according to subsequent reporting in Dark Reading, Yahoo News, and Kevin Mandia's interview with 60 Minutes broadcast in February 2021, came down to a single security analyst doing his job. A FireEye employee enrolling a new device for two-factor authentication on the corporate VPN triggered a routine alert. A security analyst noticed the same employee already had a registered device, called the employee, and learned the employee had not actually enrolled anything new. As Mandia recounted on 60 Minutes: "Our security employee called that person up and we asked, 'Hey, did you actually register a second device on our network?' And our employee said, 'No. It wasn't, it wasn't me.'"

What followed was one of the most consequential incident investigations in commercial cybersecurity history. According to Mandia's December 8, 2020 blog post, his Senate testimony of February 23, 2021, and the FireEye Form 8-K filed the same day, the attackers had stolen FireEye's Red Team penetration testing tools. and had used novel techniques to bypass the company's multi-factor authentication. Mandia's December 8 statement, which has been cited extensively, read: "We were attacked by a highly sophisticated. cyber threat actor, one whose discipline, operational security, and techniques lead us to believe it was a state-sponsored attack. Based on my 25 years in. cyber security and responding to incidents, I've concluded. we are witnessing an attack by a nation with top-tier offensive capabilities. This attack is different from the tens of thousands of incidents we have responded to throughout the years."

FireEye's analysts traced the access path back to a software supply chain compromise of the SolarWinds Orion network management platform. According to the December 13, 2020 Mandiant blog post titled "Highly Evasive Attacker Leverages SolarWinds Supply Chain to Compromise Multiple Global Victims With SUNBURST Backdoor," and according to subsequent reporting in 60 Minutes, FireEye decompiled the SolarWinds Orion code and identified roughly 4,032 lines of malicious code grafted into a trusted update. Mandiant initially tracked the activity cluster as UNC2452. before later merging it with APT29, also known as Cozy Bear, the Dukes, or, by Microsoft's nomenclature, Nobelium. According to a joint statement from the FBI, CISA, ODNI, and NSA released on January 5, 2021 and the U.S. government's formal attribution on April 15, 2021, the campaign was attributed to the Russian Foreign Intelligence Service, the SVR.

The Cybersecurity and Infrastructure Security Agency issued Emergency Directive 21–01 on the evening of December 13, 2020, the fifth such directive ever issued, requiring all federal civilian executive branch agencies to immediately disconnect or power down SolarWinds Orion software versions 2019.4 through 2020.2.1 HF1. CISA Acting Director Brandon Wales stated that "the compromise of SolarWinds' Orion Network Management Products poses unacceptable risks to the security of federal networks." Approximately 18,000 organizations had downloaded the trojanized updates, according to SolarWinds' own SEC filings, though SolarWinds later estimated. in May 2021 that fewer than. 100 customers experienced follow-on hands-on-keyboard exploitation. Confirmed affected federal agencies included the Departments of. Treasury, Commerce, State, Homeland Security, Energy. including the National Nuclear Security Administration, and Justice, where approximately three percent of Microsoft 365 email accounts were compromised according to a January 6, 2021 DOJ statement. Microsoft, Cisco, Intel, VMware, Deloitte, and NVIDIA were among the affected private sector companies, according to subsequent disclosures.

The irony was acute. FireEye had been breached. But because it caught the attack itself, decompiled the malware, and went public quickly enough to trigger a coordinated national response, the company emerged from the disclosure not as a victim but as the firm that "blew the whistle" on a Russian intelligence operation against the U.S. federal government. Mandia traveled to Fort Meade before Thanksgiving 2020 to brief General Paul Nakasone in person, a detail later disclosed at the Mandiant Cyber Defense Summit in October 2021. FireEye's share price dipped roughly seven and a half percent on the disclosure but recovered as the story developed. SolarWinds, by contrast, fell roughly 17 percent on December 14, 2020, its worst trading day since the company's 2018 IPO.

The strategic consequence of SolarWinds was that it gave FireEye and Kevin Mandia maximum leverage at exactly the moment a difficult corporate decision needed to be made. The product business was structurally challenged; the consulting and intelligence business was at the peak of its public visibility. The board had options it had not had a year earlier.

Breaking Up to Unlock Value

According to a June 2, 2021 announcement carried by CNBC, TechCrunch, and Business Wire, FireEye agreed to sell its products business, including the FireEye name, to a consortium led by Symphony Technology Group. for $1.2 billion. in cash. before taxes and transaction expenses. The remaining company would retain the consulting practice, the Mandiant Advantage threat intelligence platform, and the rights to the Mandiant brand. The board simultaneously authorized a $500 million share repurchase program. Mandia framed the rationale in plain terms in the CNBC announcement: "After closing, we will be able to concentrate exclusively on scaling our intelligence and frontline expertise through the Mandiant Advantage platform, while the FireEye Products business will be able to prioritize investment on its cloud-first security product portfolio."

The strategic logic was almost a confession. The product and services businesses had different unit economics, different sales motions, different talent profiles, and different growth trajectories. Combining them inside one publicly traded entity meant that the consulting margins dragged down the software multiple while the product growth ceiling capped the services premium. Splitting them, in theory, let public market investors and private equity owners each value the half they actually wanted to own.

The corporate rebrand to Mandiant, Inc. took effect on October 4, 2021, according to a Form 8-K filed with the SEC. The NASDAQ ticker changed from FEYE to MNDT at the open of trading on October 5, 2021. The products sale to Symphony Technology Group closed on October 8, 2021. On October 4, 2021, Mandia summed up the rebrand in Mandiant's press release: "Renaming our company as Mandiant, Inc. aligns with our mission of making every organization confident in their cyber defenses." The company that emerged was a pure-play threat intelligence and consulting business with roughly 600 consultants, more than 300 intelligence analysts, and a customer footprint across 80 countries, according to the figures Google would later cite in its acquisition disclosure.

The break-up math worked. The sum of the parts, $1.2 billion in cash from STG for products plus the eventual $5.4 billion from Google for Mandiant the following year, was meaningfully higher than the company's enterprise value as a combined entity at the time of the announcement. The lesson for boards is that, in cybersecurity at least, conglomerate structures combining hardware, software, and services rarely earn the trading multiple that any one of those businesses would earn alone.

Trellix Tries to Engineer a Second Act

Symphony Technology Group had a thesis larger than just the FireEye products business. According to a Business Wire announcement, STG had agreed in March 2021 to acquire the McAfee Enterprise business, separate from the consumer-facing McAfee Corp., in an all-cash transaction valued at $4.0 billion. According to STG's July 27, 2021 press release, that deal closed in July 2021, three months before the FireEye products sale closed in October. STG now owned two major security franchises whose product overlap was significant but whose customer bases and technology stacks were complementary, including McAfee's endpoint, secure web gateway, data loss prevention, and SIEM products alongside FireEye's network detection, sandbox, email security, and Helix offerings.

On January 19, 2022, according to SiliconANGLE, the combined entity launched under the name Trellix, a reference to a garden trellis intended to suggest, in chief executive Bryan Palma's words to VentureBeat, "living security" that "learns and adapts." Palma, according to BankInfoSecurity, had been named to lead the combined company effective with the October 2021 close, having previously served as executive vice president of FireEye's products business. after a stint as president and chief operating officer of BlackBerry. According to Wikipedia and SiliconANGLE, the new Trellix had roughly 40,000 customers, approximately 5,000 employees, and a stated annual revenue base of roughly $2 billion at inception. The XDR pitch was explicit. Palma told VentureBeat that the company aspired to be. "the market leader in XDR," ingesting telemetry from "more than 600 native and open security technologies" to provide detection and response across endpoint, network, email, and cloud.

STG made a second structural decision. According to a Business Wire announcement on March 22, 2022, STG spun out the McAfee Enterprise Security Service Edge business, which derived from McAfee's 2018 acquisition of Skyhigh Networks, as a separate company called Skyhigh Security. The initial chief executive was Gee Rittenhouse, formerly head of Cisco's cybersecurity business. According to Channel Futures, Rittenhouse left in March 2024 to become an Amazon Web Services vice president of security services, and was replaced by Vishal Rao, a former Cloudera and Splunk executive.

The pivot proved harder than the pitch. According to Channel Futures and Omdia analysis in March 2023, Trellix executed significant layoffs in 2023, with Wikipedia citing 300 to 400 employee reductions. Omdia analyst Eric Parizo wrote that "nearly the entire executive team has turned over in the last 15 months, there is a shortage of institutional knowledge regarding its legacy solutions due to departures and layoffs, and sources tell Omdia that 2023 revenue has been well below the company's estimates." Departures included chief revenue officer Adam Philpott and senior vice president of product Amol Mathur.

On January 22, 2025, according to a Trellix announcement and Business Wire coverage, STG named Vishal Rao chief executive of both Trellix and Skyhigh Security, an unusual dual-CEO structure that several analysts read as preparation for a combined sale or initial public offering. STG managing partner Marc Bala referenced Rao's track record. "leading software companies through multidimensional transformation resulting in material growth milestones and successful IPOs," a hint at exit aspirations. Bryan Palma transitioned to an STG advisor role. and was named president and chief executive of the security awareness training vendor KnowBe4 effective May 5, 2025, according to Channel Futures. In his LinkedIn statement on the move, Palma wrote that "when I joined FireEye in 2021, I had planned to lead the sale of the business and ride off into the sunset for my next operating role. Instead, over the last four years, I had the amazing opportunity to merge McAfee and FireEye and launch Trellix." As of May 2026, no Trellix S-1 has been filed publicly.

The honest assessment of Trellix is that it is the harder half of the breakup. The McAfee Enterprise endpoint installed base is large but defensive against CrowdStrike, SentinelOne, and Microsoft Defender for Endpoint. The FireEye network and email assets serve a real market but face direct competition from Palo Alto Networks, Check Point, Fortinet, and Microsoft. Trellix's XDR positioning competes with CrowdStrike Falcon Insight XDR, SentinelOne Singularity, Palo Alto Cortex XDR and XSIAM, and Microsoft Defender XDR, each backed by larger platforms with stronger telemetry advantages. A successful Trellix exit is possible, but it is engineered work rather than category creation.

Google Pays $5.4 Billion for Trust

The other half of the breakup found a different kind of buyer. Beginning in February 2022, according to a Bloomberg report dated February 8, 2022, Microsoft was in advanced discussions to acquire Mandiant. Mandiant's share price spiked as much as 18 percent on the report. On March 7, 2022, according to The Information and a subsequent Bloomberg headline that read "Mandiant Soars on Report of Google Deal; Microsoft Drops Out," Google emerged as the buyer. The deal was formally announced on March 8, 2022 in a joint press release and a Mandiant Form 8-K.

According to those filings, Google LLC agreed to acquire Mandiant, Inc. for $23.00 per share in cash, valuing the company at approximately $5.4 billion inclusive of Mandiant's net cash. The offer represented a 57 percent premium to the 10-day volume-weighted average price as of February 7, 2022, the last full trading day before market speculation about a Microsoft deal. According to CNBC, the transaction was the second-largest acquisition in Google's history behind the $12.5 billion Motorola Mobility deal in 2012, and exceeded the $3.2 billion Nest acquisition in 2014. Goldman Sachs advised Mandiant. The deal closed on September 12, 2022.

Thomas Kurian, the chief executive of Google Cloud, framed the strategic case in the joint announcement: "Organizations around the world are facing unprecedented cybersecurity challenges as the sophistication and severity of attacks that were previously used to target major governments are now being used to target companies in every industry." Mandia, in the same release, wrote that "there has never been a more critical time in cybersecurity. Since our founding in 2004, Mandiant's mission has been to combat cyber attacks and protect our customers from the latest threats." Kurian committed to retaining the Mandiant brand, a commitment he repeated when Mandia stepped down in 2024.

Mandiant joined a Google Cloud security portfolio that included Chronicle, the petabyte-scale SIEM Google had built from internal Borg-class infrastructure; Siemplify, the SOAR platform Google had acquired in January 2022 for a reported $500 million; BeyondCorp Enterprise, Google's Zero Trust offering; VirusTotal, the malware corpus Google has owned since 2012; and Security Command Center, the Google Cloud Platform-native posture management tool. The post-acquisition product roadmap merged Mandiant's threat intelligence into a unified platform marketed first as Mandiant Advantage and later as Google Security Operations and Google Threat Intelligence.

The artificial intelligence story arrived in 2024. At Google Cloud Next on April 9, 2024, according to TechCrunch and the Google Security Blog, Google announced Gemini in Threat Intelligence in public preview, layering Google's Gemini foundation model on top of Mandiant's intelligence repository to enable natural language search across frontline investigation data. Sunil Potti, the general manager of Google Cloud Security, described the offering as conversational search "across Mandiant's vast and growing repository of threat intelligence directly from frontline investigations." Gemini in Security Operations. entered general availability in the second quarter of 2024. In April 2025, according to the Google Security Blog, Google announced Sec-Gemini v1, an experimental cybersecurity model built specifically on the combination of Mandiant threat data and the Google Open Source Vulnerability data set.

Mandiant's incident response practice did not slow down inside Google. According to Cybersecurity Dive, UnitedHealth Group disclosed on February 21, 2024 that its Change Healthcare subsidiary, which processes roughly fifteen billion healthcare transactions per year and touches approximately a third of all U.S. patient records, had been breached by the ALPHV/BlackCat ransomware group via a Citrix remote access service that lacked multi-factor authentication. UnitedHealth's statement named Mandiant and Palo Alto Networks as its lead third-party consultants. According to UnitedHealth chief executive Andrew Witty's May 1, 2024 Congressional testimony, the company paid roughly $22 million in Bitcoin in ransom; approximately 100 million Americans had their health data potentially exposed.

A few months later, Mandiant identified another industry-scale campaign. According to a June 10, 2024 Google Cloud blog post, Mandiant published findings on UNC5537, a threat cluster that used credentials stolen by infostealer malware, some dating to 2020, to access Snowflake customer instances that lacked multi-factor authentication. According to subsequent reporting, approximately 165 organizations were notified as potentially exposed, with confirmed breaches at AT&T, Ticketmaster/Live Nation, Santander, LendingTree, Advance Auto Parts, Neiman Marcus, and Bausch Health. AT&T reportedly paid a ransom of approximately $370,000. Mandiant tracked an attacker reconnaissance utility it named FROSTBITE. Connor Riley Moucka was arrested in Canada on October 30, 2024, and John Erin Binns was arrested in Turkey in May 2024, according to reporting from the U.S. Department of Justice and Mandiant.

Kevin Mandia stepped down from operational leadership on May 31, 2024, according to Cybersecurity Dive. and BankInfoSecurity reporting that referenced a story originally broken by Joseph Menn at the Washington Post. He moved to an advisor role. to Thomas Kurian, remained on the board of Google Public Sector, and became a strategic partner at Ballistic Ventures, the cybersecurity-focused venture firm he co-founded. According to Mandia's own statement: "The word 'Mandiant' is now associated with the top-tier of security advisory services and incident response. It took extreme dedication to build such a strong brand." Sandra Joyce, who had worked with Mandia since 2015, took over as vice president of Google Threat Intelligence; Jurgen Kutscher took over Mandiant Consulting. Both report directly to Kurian. Kurian, in the May 2024 statement, told customers, partners, and employees: "We will continue to invest in the Mandiant organization, invest in the Mandiant brand, and nothing else will change in our day to day work."

In practice, the Mandiant brand has narrowed. Consulting and incident response retain the Mandiant name. Most software and platform deliverables have been rebranded under the Google Security Operations and Google Threat Intelligence umbrellas. That is the natural outcome when a strategic acquirer integrates a respected boutique into a much larger platform with its own brand equity.

Lessons for Founders

The first lesson, and the one most painful for technical founders to internalize, is that being right about the technology is the easy half of the problem. Ashar Aziz built one of the first commercially successful behavior-based detection engines at a moment when signature-based antivirus was demonstrably failing against state-sponsored adversaries. The technology was correct. According to the FireEye S-1 and the subsequent customer base, the product was sold to financial institutions, defense contractors, and intelligence agencies precisely because no competing approach worked at the time. None of that protected the company from the fact that the underlying delivery model, expensive on-premises appliances with three-to-five-year refresh cycles, was about to be made structurally obsolete by cloud-delivered software.

Innovation is necessary but is not sufficient. The founder who insists that the product is the moat, without equal attention to how that product is sold, deployed, updated, and renewed, has only solved one of the two hard problems. Ashar Aziz, on a 60 Minutes panel in 2014, was vindicated as a visionary. Eight years later, when his company sold off the products half for $1.2 billion, the vindication was technical only. The commercial vindication went to George Kurtz at CrowdStrike, who had not invented sandbox detection but who had built a cloud-native single-agent architecture from day one.

The second founder lesson concerns the trade-off between being early and being too early. According to public records of FireEye's product launches and revenue ramp, the company was selling production sandbox appliances by 2008 and 2009. CrowdStrike did not ship Falcon until June 2013. FireEye had a four-to-five-year head start. That head start translated into a category-defining brand, an early IPO, and a peak market value above $15 billion. It did not translate into a durable platform position, because the platform was built around hardware delivery that became expensive ballast as cloud adoption accelerated. A founder building a category-defining technology must constantly ask whether the delivery model that earned the first hundred customers will also serve the next thousand. If the honest answer is no, the platform transition must begin well before financial pressure forces it.

The third founder lesson concerns when to step aside. Ashar Aziz made the right call. According to FireEye executive biographies filed with the SEC, he handed the chief executive role to David DeWalt in November 2012. and moved into a chief technology officer and chief strategy officer role. The IPO that followed in September 2013, priced by Morgan Stanley with co-managers Goldman Sachs, JPMorgan, and Barclays, would have been substantially harder to execute under a deeply technical founder unfamiliar with the public market choreography. Aziz's choice to bring in a former McAfee chief executive at exactly the moment FireEye needed to scale into the enterprise was correct on its own terms. The deeper question is whether subsequent strategic choices, particularly the decision to lean into appliance economics and acquire a services business rather than pivot to cloud delivery, were the right ones; that is a board-level rather than founder-level question, addressed below.

The fourth founder lesson concerns cultural integration after services-plus-products acquisitions. According to Forrester analysis, Omdia commentary, and the documented post-deal personnel attrition, the FireEye-Mandiant merger never produced a unified culture. The two halves had different incentive structures, different self-conceptions, and different motions. Founders contemplating similar transactions should plan, before signing, for the operational reality that consultants and software sellers do not naturally cohabit. The transaction can still create value, but the integration cost must be modeled honestly. In FireEye and Mandiant's case, eight years after the merger, the value was unlocked not by integration but by separation.

Lessons for Boards and Investors

The first board-level lesson is to read product revenue mix carefully and act on the signal early. According to FireEye's 10-K filings, product revenue peaked at $216.6 million in 2015 and fell to $151.9 million in 2016, even as total revenue continued to grow on the strength of services and subscription. That was the visible signal that the appliance business was in absolute, not just relative, decline. Boards in similar positions should treat declining product revenue inside a growing top line as a strategic flashing light, not a margin issue to be solved with operating discipline. The implication is not necessarily that the company should be sold or restructured immediately; it is that the leadership team must be able to articulate the platform transition path in concrete, dated terms, and the board must be willing to fund the cannibalization that path requires.

The second board lesson concerns recognizing platform shift risk in time to do something about it. CrowdStrike launched Falcon in June 2013. By 2015 and 2016, according to reseller surveys and customer reports, CrowdStrike was actively displacing FireEye-adjacent vendors at large enterprise accounts. By the time FireEye's board acted to transition the company under Kevin Mandia in 2016, the structural disadvantage was already well established. Boards in cyclical platform shifts have a narrow window, typically eighteen to thirty-six months from the appearance of the disruptive architecture, in which decisions about cannibalization, acquisition, or even sale will determine the company's terminal value. Acting in year five is generally too late.

The third board lesson concerns the premium versus growth trade-off. FireEye chose, under DeWalt, to position itself as the premium APT detection platform. That positioning was strategically defensible when the threat was novel and the customer set was narrow. It became commercially difficult when sandbox functionality became a feature inside next-generation firewalls and endpoint platforms, and when the buyer set broadened beyond intelligence agencies and Fortune 100 banks. Premium positioning in cybersecurity is a temporary state, not a durable strategy. The market commoditizes detection capabilities at a predictable pace, typically three to five years from category creation to next-generation firewall integration. Boards should pressure-test premium pricing strategies against the question of what happens when the feature ships in a competitor's platform for free.

The fourth board lesson concerns when to break up versus when to fight. In retrospect, the 2021 split was the correct decision; the math worked. STG paid $1.2 billion for the products business that was structurally challenged, and Google paid $5.4 billion the following year for the consulting and intelligence business that was at the peak of its public visibility post-SolarWinds. The combined $6.6 billion gross was meaningfully higher than the company's enterprise value as a combined entity at the time of the announcement, and substantially higher than reasonable consensus on what the combined entity would have fetched in a single transaction. Boards facing a similar architecture, a respected services or intelligence brand sitting inside a struggling product business, should consider sum-of-parts analysis as a serious strategic option before defaulting to operational fixes that have repeatedly failed to close the multiple gap.

The fifth board lesson, and perhaps the most counterintuitive, is that crisis can create strategic optionality. The SolarWinds disclosure in December 2020 was, on its face, the worst kind of news for a cybersecurity vendor: the company itself had been breached. Yet because FireEye caught the attack, disclosed it transparently, and led the public response, the disclosure became a brand asset rather than a brand liability. According to subsequent press accounts, the perceived integrity of the response gave Mandia personal credibility with U.S. government officials, with customers, and with the public market. That credibility translated directly into negotiating leverage in the 2021 split and the 2022 Google sale. Boards should not engineer crises, but they should recognize that a well-handled crisis can shift the strategic option set.

Lessons for Product and Strategy Leaders

For product and strategy leaders, the first conclusion is structural: appliance-based security is finished as a stand-alone category. According to the trajectory of every major sandbox-era vendor, including Damballa, Cyphort, Lastline, Bromium, Cylance, Carbon Black, and FireEye itself, the appliance and on-premises delivery model has not produced a single durable independent franchise outside of vendors that were already platform companies (Cisco, Check Point, Palo Alto Networks, Fortinet) with diversified portfolios able to absorb the architectural transition. The strategic implication for any product leader weighing a new security category is that the default delivery model is cloud-native single-agent or API-integrated, and any deviation from that default requires an explicit justification.

The second product lesson concerns telemetry as moat. CrowdStrike's Falcon platform did not win because its detection logic was superior to FireEye's; the malware research communities at both firms were comparably strong. Falcon won because every endpoint streamed telemetry to a shared cloud back end that grew more capable with each new customer. That data network effect is the genuine moat in modern cybersecurity. Product leaders should design from day one for telemetry concentration, not as a future capability but as the architectural premise. A security product that collects data only on customer premises, or that returns only sampled metadata to the vendor, is structurally disadvantaged against a competitor that collects all of it.

The third product lesson concerns the relationship between detection and prevention. FireEye's original pitch was prevention through pre-execution sandbox detonation. The market has since moved toward an integrated model in which prevention, detection, and response are functions of the same platform, with the operational center of gravity at detection and response rather than prevention. Endpoint detection and response, extended detection and response, managed detection and response, and security operations platforms have all converged on the idea that breaches are inevitable and that the differentiator is the speed and quality of the response. Product leaders should explicitly architect for the post-breach world.

The fourth product lesson concerns the difference between threat intelligence as moat and threat intelligence as product. Mandiant's threat intelligence was a competitive moat because it was generated as a byproduct of frontline incident response. The intelligence came from cases that Mandiant consultants actually worked. That kind of intelligence is hard to replicate because it requires the consulting practice that generates it. The lesson for product leaders is that selling threat intelligence as a stand-alone product, divorced from a frontline incident response practice or a large telemetry footprint, is structurally weak. iSIGHT Partners, the firm FireEye acquired for up to $275 million. in 2016, struggled in part because it lacked the deep operational substrate that Mandiant's intelligence team had.

The fifth product lesson concerns unit economics and the gap between appliance and SaaS delivery. The capital intensity of selling, shipping, deploying, and refreshing appliances is structural. According to public filings, FireEye's gross margins on subscription and services revenue trended into the 60 to 70 percent range, while product gross margins on appliances were comparably high but at the cost of significant inventory, channel, and deployment overhead. CrowdStrike's subscription gross margins, according to recent 10-K filings, run in the high 70s. after stripping out professional services. The compounding effect over a decade of growth is enormous: every dollar of revenue at CrowdStrike funds more research and development, more sales hiring, and more product velocity than every dollar of revenue at an appliance-based competitor. Product leaders weighing architectural choices should model the long-run consequence of structural margin differentials before optimizing the first product release.

What FireEye, Mandiant, and Trellix Teach About Being Right and Losing

The clean way to state the case study is this. FireEye, Mandiant, and Trellix are three companies that proved you can be technically vindicated, professionally respected, and commercially defeated at the same time, and that the third condition does not erase the first two but it does determine the financial outcome. The technology Ashar Aziz invented in 2004 detects threats that signature-based antivirus still cannot reliably catch in 2026. The framework Kevin Mandia and his team imposed on Chinese nation-state activity in February 2013 with the APT1 report is the framework that intelligence agencies, regulators, and enterprise CISOs still use to discuss adversaries. The incident response practice Mandiant built remains the firm that the largest companies in the world call when something has gone catastrophically wrong, as UnitedHealth and Snowflake's customers confirmed in 2024.

What the case study teaches is that none of those forms of correctness produced the commercial outcome a public market investor would have expected at the company's 2014 peak. Three structural choices determined the gap. The first was the choice to monetize the technology through expensive on-premises appliances at exactly the moment the broader enterprise was migrating to the cloud. The second was the choice to acquire a services and intelligence business and run it inside a product company without successfully integrating the two cultures or the two business models. The third was the choice, perhaps inevitable given the first two, to spend the second half of the 2010s defending a position that the market had structurally moved past, rather than aggressively cannibalizing the appliance business in favor of a cloud-delivered architecture. CrowdStrike, founded in 2011 by an executive who had watched the same market dynamics from inside McAfee, made the opposite choice on all three counts and built one of the most valuable software franchises of the 2020s.

The afterlife is instructive. Mandiant lives inside Google, where its consultants still take the call when the largest breaches happen and its intelligence feeds the Gemini-powered conversational search that Google now sells across its Cloud security portfolio. Trellix is in the harder spot, a private equity portfolio company attempting a second-act XDR pivot against three larger and better-capitalized competitors, with executive turnover, layoffs, and an opaque path to public market exit. The brand that Ashar Aziz built, FireEye, no longer exists as an independent product line; the brand that Kevin Mandia built, Mandiant, survives inside the world's third-largest cloud provider as a service practice and a wrapped intelligence offering.

For founders, the operational implication is to design the delivery model with the same rigor as the technology. For boards, the implication is to read mix shifts and platform shifts early, and to consider sum-of-parts seriously when the integrated whole is trading at a discount. For product and strategy leaders, the implication is that telemetry concentration, cloud-native delivery, and integration of detection and response are now the table-stakes premises against which any new security product will be measured. The case of FireEye, Mandiant, and Trellix is the most expensive demonstration in modern cybersecurity that being technically right and being commercially right are different problems, that solving the second one requires choices the first one does not force, and that the company that solves both wins the entire market.