April 16, 2026

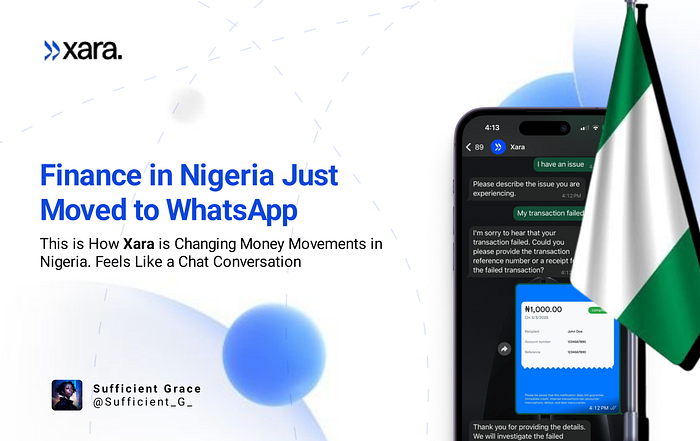

Finance in Nigeria Just Moved to WhatsApp

How Xara is Changing Money Movements in Nigeria. Feels Like a Chat Conversation

Sufficient Grace

27 min read

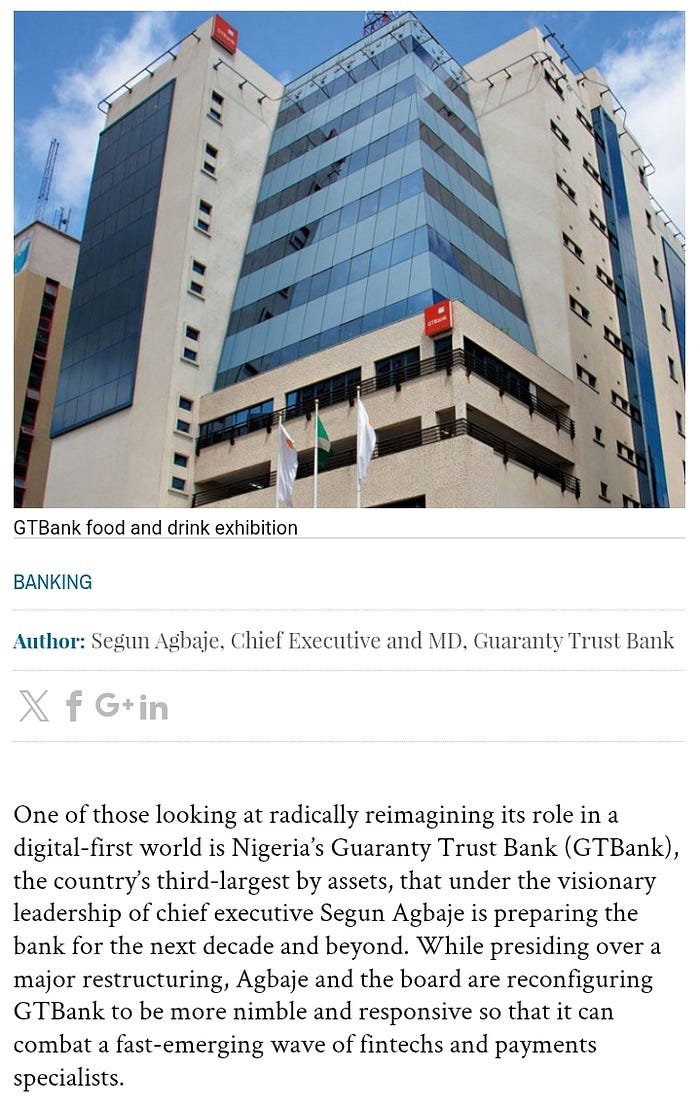

The evolution of electronic banking in Nigeria reflects a broader shift from branch-based banking to digital financial services, driven by regulatory changes, FinTech growth, and innovation across commercial banks. Within this transition, Segun Agbaje, as CEO of Guaranty Trust Bank, led one of the banks that became widely recognized for early adoption of digital banking tools and customer-focused financial technology solutions during this period of industry transformation. During that period, banking in Nigeria was still heavily dependent on physical interaction. Customers were required to visit bank branches for even the simplest transactions, such as transfers, account inquiries, and bill payments. The system was slow, manual, and often inconvenient. However, as technology began to reshape global finance, expectations around speed and accessibility started to change, pushing banks to rethink how services were delivered. Under Segun Agbaje's leadership, GTBank positioned itself as one of the early adopters of digital banking in Nigeria. The bank invested significantly in electronic channels such as internet banking, ATM systems, and card-based payment solutions. These innovations were not just about introducing new tools, but about changing how customers interacted with their bank. The goal was clear: reduce friction, improve convenience, and allow users to carry out financial transactions without necessarily visiting a physical branch.

This approach played an important role in shaping customer expectations in Nigeria's banking sector. As more users became exposed to digital banking systems, the demand for faster, more seamless financial services increased. Banking gradually shifted from a branch-centered model to a service model where accessibility and user experience became key competitive factors. In a broader sense, this period represents how traditional banks responded to the early wave of digital transformation before the rise of modern Fintech companies. While Fintechs later accelerated innovation, incumbent banks like GTBank were already laying the foundation by introducing digital infrastructure and encouraging customers to adopt electronic banking behaviors. Today, as conversations around open banking, artificial intelligence, and conversational finance continue to grow, the impact of that early digital transition is still visible. It marked the beginning of a long shift in Nigerian banking, from physical processes to digital ecosystems, and from institution-centered banking to customer-centered experiences. However, despite the widespread acceptance of e-banking in Nigeria, many challenges still prevent consumers from fully utilizing these services and achieving maximum satisfaction. These challenges range from human limitations to operational inefficiencies and technical constraints

THE ADOPTION OF ELECTRONIC BANKING IN NIGERIA

E-banking in Nigeria began in the 1980s and gained momentum with the emergence of "new generation" banks. A key development during this period was the establishment of Diamond Bank (now Access Bank) Plc, which introduced online real-time interconnectivity that helped popularize electronic payments nationwide. This innovation significantly increased competition among banks, forcing many of them to adopt electronic payment systems in order to remain competitive. It also allowed banks to showcase their products and services through digital platforms such as websites, marking a shift toward modern banking practices. Electronic banking continued to evolve through several stages of development. The earliest form of e-payment systems in Nigeria included Magnetic Ink Character Recognition (MICR) cheques, followed by the introduction of Automated Teller Machines (ATMs) in the early 1990s. These ATMs enabled customers to withdraw cash, check balances, and pay for utilities without visiting bank branches.

In 1993, the Central Bank of Nigeria introduced smart card technology, further advancing electronic payment systems. By 2003, the Central Bank issued formal guidelines on e-banking, clearly defining operators, agents, products, and service channels within the system. The growth of e-banking was further strengthened by the introduction of infrastructure such as the Inter-switch system in 2004 and the Nigerian Inter-Bank Settlement System (NIBSS) Electronic Fund Transfer (NEFT). These innovations improved interbank transactions and made electronic payments more efficient and widely accessible. According to the Central Bank of Nigeria Economic Report of 2008, the use of electronic payment systems continued to grow rapidly, driven by increased public awareness and aggressive marketing by banks. ATMs remained the most widely used channel, accounting for about 87% of electronic banking transactions, while Point of Sale (POS) terminals accounted for the least usage at 2.5%.

Nigeria has one of the fastest-growing digital financial ecosystems in Africa, with a population of approximately 220 million people, and an estimated 110–130 million financially active, Nigeria has 80 to 110 million people already using some form of e-banking, from traditional bank apps to fintech platforms like OPay, PalmPay, and Moniepoint. • OPay has over 50 million+ downloads and users. • PalmPay has about 35 million+ registered users. • Moniepoint has over 10 million+ users and businesses. Combined, the fintech ecosystem in Nigeria has an estimated 60–80 million active users when overlaps are removed. Overall, studies suggest that about 96% of Nigerians use at least one form of digital financial service, including bank apps, fintech platforms, USSD, and POS systems.

THE PROBLEM WITH E-BANKING IN NIGERIA

Despite this growth, the adoption of e-banking in Nigeria is constrained by several challenges, which are broadly categorized into human, operational, and technical constraints. The core issue is not availability of services, but the difficulty people face when actually trying to use them in real life.

One major problem is usability and complexity. Most banking and fintech apps require multiple steps, technical inputs, and structured navigation. For users who are not digitally skilled, or who are simply trying to complete a quick transaction, this becomes frustrating and time-consuming. What should be simple money movement often feels like a process.

Another major issue is financial literacy and accessibility. A large portion of users are not fully comfortable with formal financial language or complex digital interfaces. Elderly users, low-literacy users, and people with visual or physical limitations often struggle with small text, multi-step authentication, and app-heavy workflows. This creates a silent exclusion even when services are technically "available."

On the infrastructure side, network instability and system downtime remain challenges. Failed transactions, delayed confirmations, and inconsistent performance across platforms reduce user confidence in digital banking. Even when systems work, reliability is not always guaranteed.

The system is fragmented across multiple platforms. Users often switch between bank apps, Fintech apps (like opay, PalmPay, etc), USSD codes, and agents just to complete simple financial tasks. This lack of a unified experience creates unnecessary friction in everyday money movement. The full potential of e-banking in Nigeria is still limited by human, operational, and technical challenges. Addressing these issues, especially infrastructure gaps, security concerns, and user accessibility, will be essential for ensuring the continued growth and sustainability of e-banking in Nigeria.

ENTER XARA: Making Everyday Banking Simple on WhatsApp

This is where the shift happens. Xara, built by Xava technologies aims to solve the problem of complex, fragmented, and inaccessible banking experiences in Nigeria.

It focuses on removing the friction in sending money, converting stablecoins to naira, navigating multiple apps, and dealing with risky P2P exchanges, by bringing everything into a simple, conversational flow inside WhatsApp.

Let's break it down….

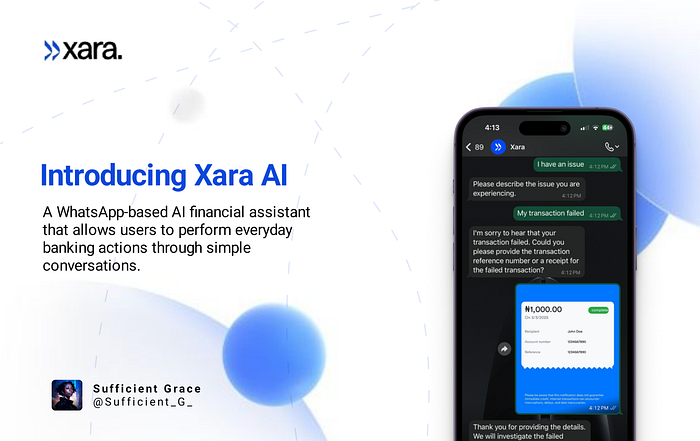

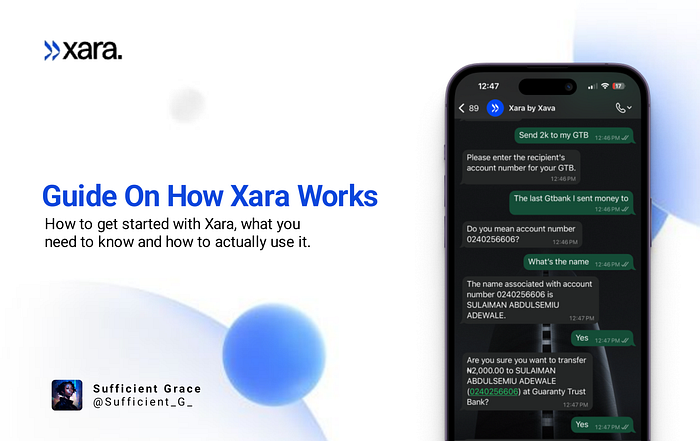

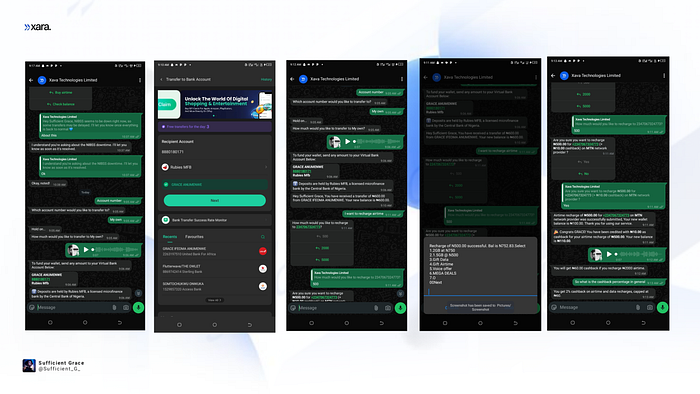

Xara is a WhatsApp-based AI financial assistant that allows users to perform everyday banking actions through simple conversations instead of traditional banking apps or USSD codes. It is a system that lets you send money, pay bills, check spending, and manage basic financial tasks by chatting, sending voice notes, or sharing images on WhatsApp, just like you would talk to a person. Rather than requiring users to open a banking app, navigate menus, or manually enter account details, Xara translates natural language into financial actions. For example, you can say or type "Send ₦50,000 to Sufficient Grace for lunch," and the system processes the request through connected banking infrastructure after confirmation and security verification.

Xara routes transactions through banking rails that allow interoperability with 50+ Nigerian banks, meaning you can send money across most major banks directly from WhatsApp without switching apps.

Xara is also designed to support stablecoin-based deposits, including assets like USDC and USDT, through supported blockchain networks, especially the Solana network. When you deposit stablecoins such as USDC or USDT via the Solana network, the system automatically processes the transaction in the background. Once the funds arrive, Xara automatically converts the stablecoins into naira. You do not need to manually swap, trade, or interact with any exchange interface. Everything happens inside the system. You don't need to search for merchants, or to check exchange rates. You just receive, deposit, and continue using your money directly inside WhatsApp in naira.

Xara uses AI to understand how people naturally communicate, whether through text, voice notes, or even images, and turns those messages into real financial actions like sending money, receiving payments, and checking spending.

But it is not just an AI tool on its own. It combines AI with payment systems, stablecoin support, and financial infrastructure to actually move money, not just respond to messages.

Xara is designed specifically for the Nigerian context, where WhatsApp is widely used across different age groups, professions, and income levels. This makes it accessible even to users who may not be comfortable with formal banking applications or complex digital interfaces. It also supports voice notes and local communication styles, which helps reduce literacy barriers and improves ease of use.

Xara is where AI meets banking inside WhatsApp, making financial actions feel like everyday conversation. Public reports show early traction: • Around 10,000 users in early rollout phase. • About ₦135 million+ in transaction volume shortly after launch in June 2025.

This shows early adoption is driven more by curiosity + convenience than marketing.

WHY WHATSAPP? WHY NOT IT'S OWN APP?

Xara uses WhatsApp instead of building a standalone app because the goal is not just to deliver financial services, but to remove the friction that usually comes with accessing them. In Nigeria, the biggest barrier in digital finance is not awareness, it is effort. Users already struggle with downloading multiple apps, learning new interfaces, and trusting unfamiliar systems. By building on WhatsApp, Xara enters an environment where users are already active, already comfortable, and already communicating daily.

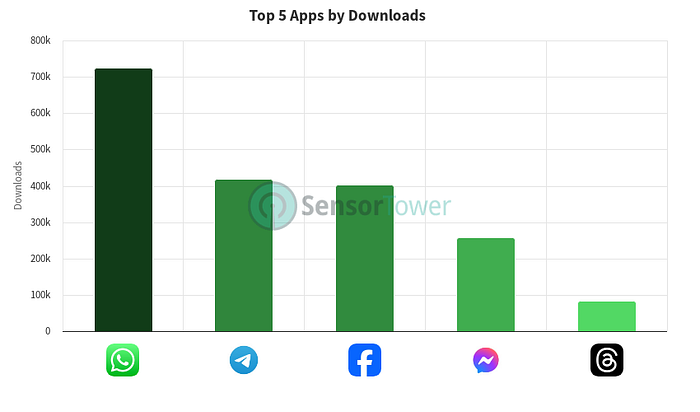

WhatsApp stands out from other social platforms because it is fundamentally a utility, not just a content platform. Unlike Instagram, TikTok, Facebook, or X, which are driven by content consumption, discovery, and social engagement, WhatsApp is primarily used for direct communication. It has 51M+ users in Nigeria, and almost everyone online uses it , which is why building financial tools inside it makes sense. This makes it more functional and action-oriented. People use it to talk to family, coordinate business transactions, share important information, and make decisions in real time. This "utility-first" behavior makes it a natural fit for financial actions, where clarity and direct interaction are more important than entertainment or content browsing. When compared to platforms like Instagram and TikTok, the difference becomes even clearer. Instagram and TikTok are highly visual and algorithm-driven platforms designed to maximize engagement and content consumption. They are not structured for structured tasks like banking, payments, or financial decision-making. Users go there to scroll, not to execute tasks. Similarly, X (formerly Twitter) is primarily built around public conversations, opinions, and information flow, not private financial interactions. Facebook, while more utility-oriented than TikTok or Instagram, is still centered around social networking and content feeds rather than real-time conversational transactions. WhatsApp, on the other hand, operates in a private, one-on-one or group messaging environment. This creates a sense of control, familiarity, and trust. Users are not distracted by algorithms or content feeds. They are simply communicating, and can function during low networks. This makes it easier to introduce structured actions like sending money, paying bills, or checking balances within a natural conversation flow. For a system like Xara, which relies on understanding intent and executing financial actions, this environment is significantly more aligned with user behavior. Another important factor is accessibility. WhatsApp is widely used across different demographics in Nigeria, including traders, students, professionals, and rural users. It also performs well on low-end smartphones and requires less data compared to content-heavy platforms. This makes it more inclusive, especially in a market where device limitations and network instability are still common challenges.

In contrast, other platforms often require strong network, higher data consumption and are less consistent in supporting structured, task-based interactions. They are designed for attention, not execution. WhatsApp, however, sits in a unique position where communication and action overlap, making it ideal for embedding services like financial transactions. In summary, WhatsApp was chosen because it is not just a social platform, it is already a behavioral infrastructure for daily communication. Compared to Facebook, Instagram, TikTok, and X, it offers a simpler, more direct, and more trusted environment. For Xara, this means users do not need to learn a new system; they only need to continue doing what they already do, chat, while financial actions are seamlessly executed within that flow.

FEATURES OF XARA

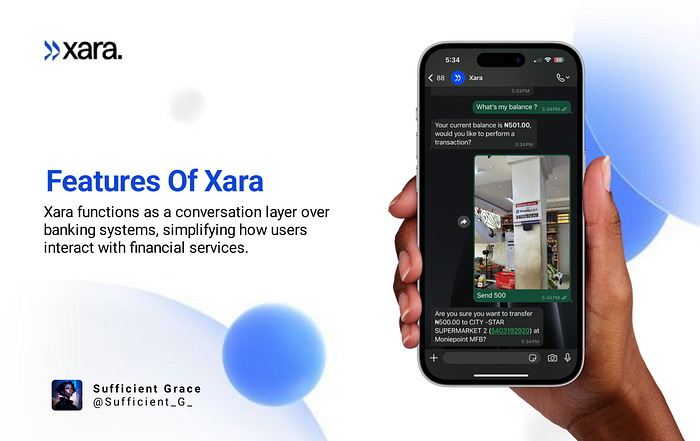

At its core, Xara functions as a conversation layer over banking systems, simplifying how users interact with financial services. Instead of replacing banks, it sits on top of existing banking infrastructure and makes it easier for people to access and use it in their daily lives:

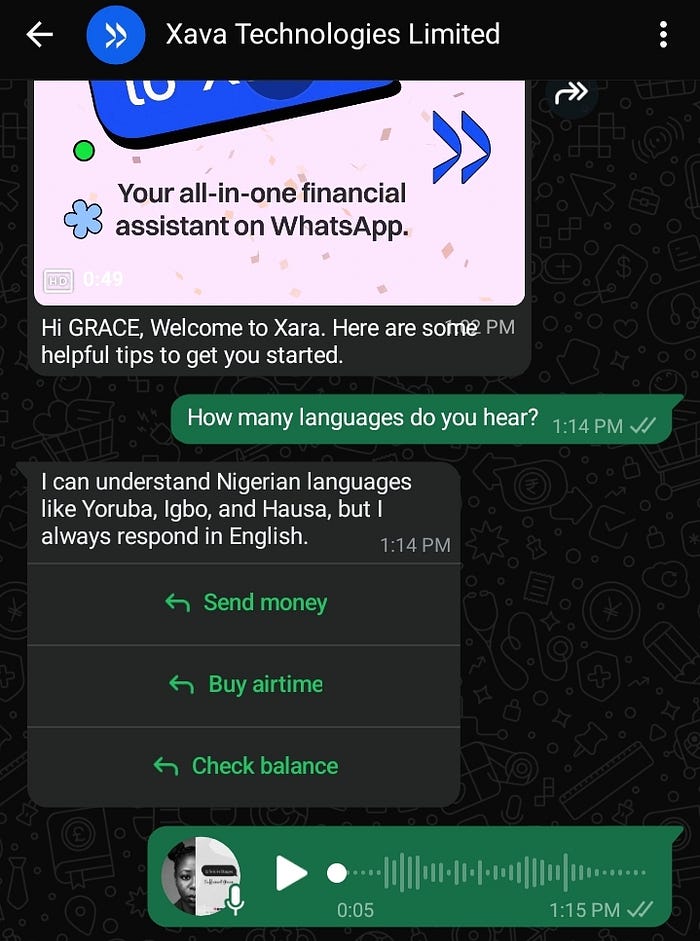

1. Conversational Banking Xara allows you to perform financial actions by simply chatting on WhatsApp. Instead of navigating menus or apps, you just type or speak commands like "send money" or "pay bills," and the system understands and executes them. 2. Voice Note Support You can send voice notes instead of typing. Xara can interpret spoken instructions in natural speech, including Pidgin English and other local expressions, making it easier for people who prefer talking over typing. 3. Multilingual Understanding Xara supports different communication styles, including English, Nigerian Pidgin, and local language like Igbo, Yoruba and Hausa expressions. This makes it more inclusive for users across different backgrounds and literacy levels. 4. Image Recognition You can upload pictures of bills, account numbers, or receipts. Xara extracts the relevant information from the image and uses it to complete transactions, reducing manual input errors. 5. Money Transfers Xara enables instant money transfers between bank accounts or within its network. You can receive USDC/USDT using wallet address and Naira using account number, you can send Naira using just a name, phone number, or simple instruction in chat form. Xara only allows stablecoin transfers (USDC/USDT) between users on its platform. This means you can only send to another Xara user using their Xara-linked WhatsApp number. If the person is not on Xara, the transfer won't go through. 6. Bill Payments and Utilities You can pay for services such as electricity, airtime, and data directly through chat. This removes the need to switch between multiple apps or platforms. 7. Spending Insights Xara provides summaries of your spending habits. It shows how money is being used over time, helping you understand their financial behavior more clearly. 8. Smart Memory The system remembers past conversations and transactions. This allows you to refer back to previous actions using simple phrases like "send again" without repeating details. 9. Security and PIN Protection Every transaction requires a secure PIN confirmation. This ensures that no financial action is completed without user approval, adding a layer of safety and control. 10. Fast Onboarding You can start using Xara directly on WhatsApp without downloading a separate app. Registration and verification are done inside the chat, making the process quick and simple. 11. Works on Low-End Devices Because it runs on WhatsApp, Xara does not require high storage space or powerful smartphones. It works smoothly even on basic devices with low internet speed.

12. Referral Code

There is also a referral system, where users can unlock referral access after completing a few transactions and earn rewards when others join and use the platform.

WHY THESE MATTERS?

In the Nigerian e-banking system, many of the challenges people face are not just about technology. They are human. They come from the everyday realities of how people see, read, understand, and interact with systems. This is the gap that solutions like Xara are beginning to address, not by changing the system itself, but by changing how people experience it. 1. One major problem is language and expression. Many Nigerians are more comfortable speaking in their native language, but banking systems force formal English.

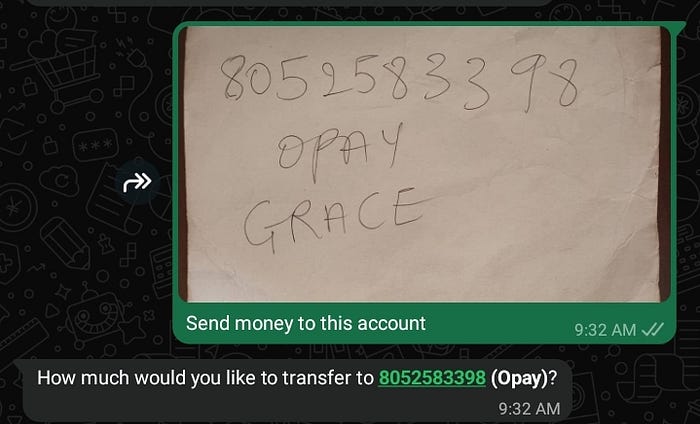

With Xara, users can speak naturally: • Igbo: "Ziga ₦5,000 nye Chinedu" • Yoruba: "Fi ₦10,000 ranṣẹ si Tunde" • Hausa: "Aika ₦3,000 zuwa Musa" • Pidgin: "Send 2k give Emeka" Xara understands all of this and responds in clear English, so the user doesn't need to struggle with formal banking language. 2. Another issue is visual stress and poor eyesight. Small texts, bright screens, and long account numbers make transactions hard. Xara reduces this: • Send a voice note instead of typing • Snap a picture of an account number or bill • Send it → Xara reads it → you confirm

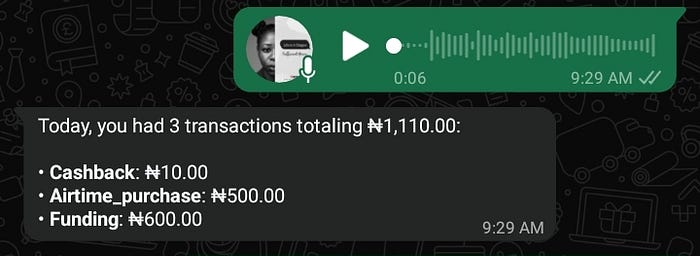

No need to strain your eyes or type everything manually. 3. Then there is complexity and too many steps. Traditional banking means switching apps, entering details, confirming, going back and forth. With Xara: • "Send ₦5,000 to John" • "Pay my NEPA bill" • "Buy airtime ₦1,000" Everything happens inside one chat. No switching, no multiple screens, no long process. 4. Another problem is tracking and understanding spending. Many people don't have a clear picture of where their money goes. To get proper records, some go to the bank to print statements, while others keep checking different apps over and over. Even then, the breakdown is not always clear. With Xara, this becomes simple. You can just ask: • "How much did I spend on airtime this month?" • "Show my food expenses" • "Where is my money going?"

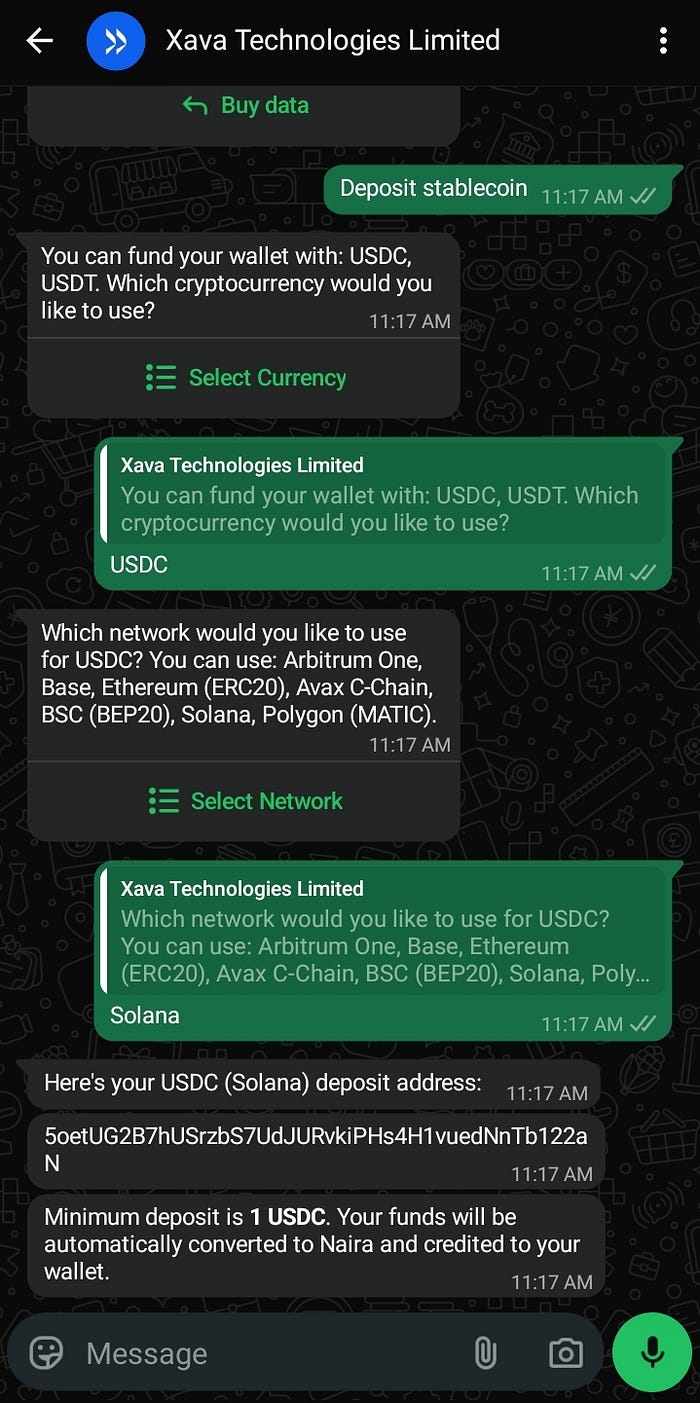

Xara gives you a clear breakdown instantly. It also helps you build records automatically. NB: When sending money, you can add small descriptions like: • "₦5,000 for food" • "₦10,000 transport" Over time, Xara uses this to organize your spending and give you insights without you doing the work. No manual calculations required. You don't need to go to the bank, or keep juggling multiple apps. You just ask, and it tells you. 5. Many Nigerians earn in stablecoins like USDC and USDT, but they often face a major challenge when converting them to naira. The process usually depends on P2P merchants, which exposes users to delays, unfair rates, and in some cases, fraud or outright loss of funds. This creates unnecessary risk in something that should be simple: receiving money and converting it safely into local currency. Xara removes this friction by automating the entire conversion process inside WhatsApp and reducing dependence on risky P2P interactions. Here is how the stablecoin deposit flow works: • First, you tell Xara that you want to deposit stablecoins. Like "Hi Cara, deposit stablecoin." • Xara then responds by asking which asset they want to deposit, USDC or USDT. • After selecting the stablecoin, Xara asks the user to choose a network. The user selects available network like Solana. • Once confirmed, Xara generates a wallet address for the deposit.

You then share this wallet address with whoever is sending the stablecoins. Once the funds are sent and confirmed on-chain, the deposit automatically reflects inside the Xara chat interface. Immediately after confirmation, the stablecoins are converted into naira and credited to the user's balance. In simple terms, users move from stablecoin to naira in one clean flow, without P2P negotiation, without manual conversion, and without exposure to third-party fraud risks. Xara makes banking simple by turning it into a conversation inside WhatsApp. It has about 45,000 users. And has processed around ₦8 billion in total transactions since launch.

XARA x SOLANA INTEGRATION

Xara integrates with the Solana ecosystem in a way that focuses on speed, cost efficiency, and real-world usability. Solana matters in this setup because it provides fast transaction finality and very low fees. This allows Xara to process stablecoin movements quickly without delays or high costs, which is important for everyday financial use cases like sending money, paying bills, or receiving funds.

The value of fast, low-cost blockchain infrastructure,like Solana, comes down to one thing: making financial services actually usable in real life.

Speed matters because people don't want to wait minutes or hours for transactions to go through. Whether it's sending money, receiving payments, or converting funds, users expect it to happen instantly. Fast infrastructure makes real-time finance possible.

Low cost is just as important. High transaction fees make small payments impractical, especially in everyday situations like buying food, paying transport, or sending small amounts to family. When fees are almost negligible, people can transact freely without worrying about losing value.

It also improves efficiency. A system that can handle many transactions at once without slowing down ensures reliability, especially as more users come in. This is critical for platforms like Xara, where multiple users are interacting at the same time.

It enables better financial access. With faster and cheaper infrastructure, users can move money across borders, convert currencies, and access digital finance without going through complex or expensive intermediaries.

In simple terms, fast and low-cost blockchain infrastructure removes delays, reduces costs, and makes financial products smoother and more practical for everyday use.

For the platform itself, Solana reduces friction in settlement. When users deposit stablecoins like USDC or USDT, the network enables fast confirmation and smooth backend processing. This helps Xara deliver near-instant conversion and transaction completion inside WhatsApp without exposing users to blockchain complexity. Xara increases real-world usage of Solana-based stablecoin transfers. It brings non-technical users into crypto rails without requiring them to understand wallets or blockchain mechanics. This expands transaction volume and utility for Solana beyond trading and DeFi use cases. To be honest, Xara is deeply integrated with Solana campaigns including bounty programs, builders connect, etc. These initiatives are designed to keep the community active, encourage education around the product, and drive real usage. Through bounties and community engagement, users and builders are incentivized to participate, test features, and share real-world use cases. The goal is simple: strengthen adoption by combining product usage with continuous community participation within the broader Solana ecosystem. Overall, the integration benefits both sides: Solana provides the infrastructure for fast and cheap settlement, while Xara turns that infrastructure into a simple, chat-based financial experience that ordinary users can actually use.

STEP-BY-STEP GUIDE ON HOW XARA WORKS IN PRACTICE

I'm going to show you how to get started with Xara, what you need to know and how to actually use it.

Not just the basics, but how to move from opening a chat to actually sending money, receiving funds, depositing stablecoins, and keeping track of your spending without confusion.

You'll see how to interact with Xara using normal messages or voice notes, how transactions are confirmed, and how everything happens directly inside WhatsApp without switching apps.

By the end, you should be able to use Xara confidently for everyday things, sending money, receiving payments, and managing your finances in a way that feels natural.

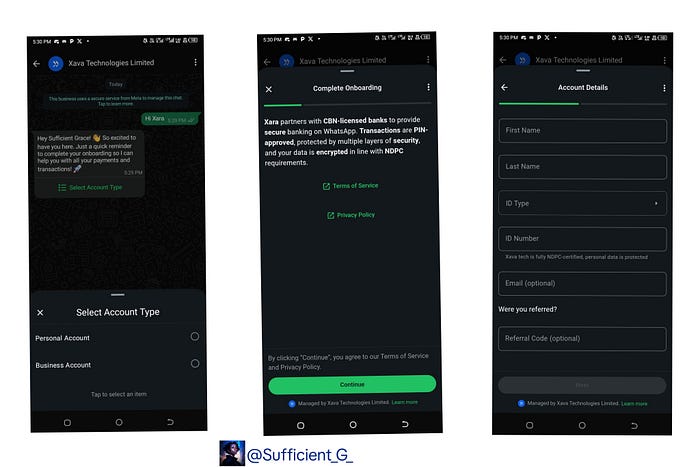

Step 1: Start the conversation on WhatsApp • You begin by visiting Website: www.usexara.ai • Click on 'Try Xara now' to direct you to WhatsApp and message Xara the official chat number during onboarding.

At this stage, there is no app download, or complex setup screen. The entire system begins like a normal chat conversation Step 2: Account creation and verification Once the chat starts, Xara guides the you through a simple onboarding flow. You will be asked to provide basic details such as: • Full name • Home Address • NIN or BVN for KYC compliance

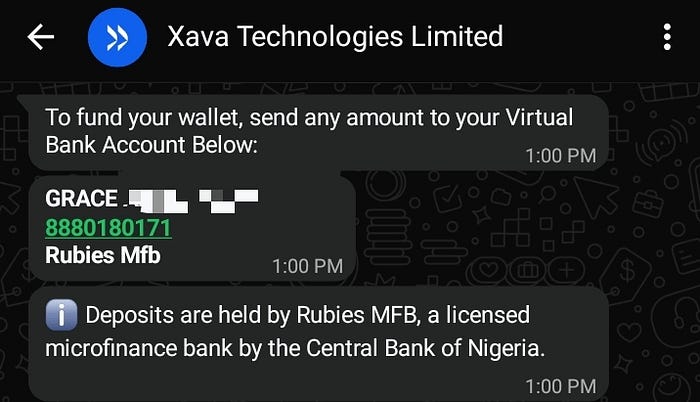

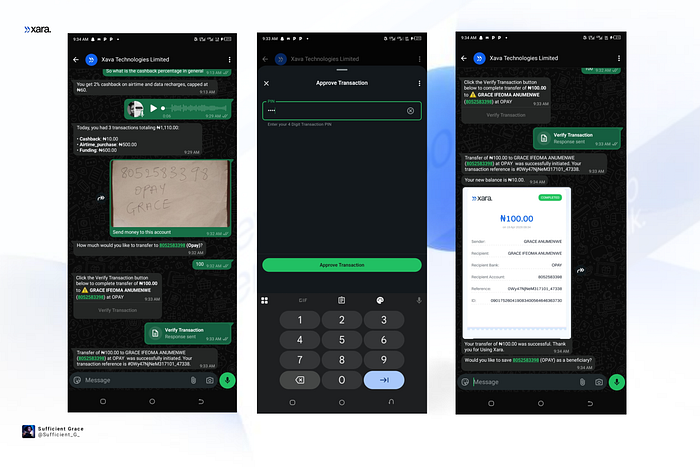

This step connects you to Nigeria's financial infrastructure and ensures identity verification in line with regulatory requirements. Step 3: Set up security PIN After verification, you will be directly to create a 4-digit transaction PIN. This PIN becomes the key security layer for: • sending money • paying bills • approving financial actions Every transaction requires this confirmation before execution. Do not show your transaction PIN to anyone. Step 4: Link financial access (bank integration) Xara connects to your bank account through integrated banking rails and partners (including multiple Nigerian banks and payment infrastructure). It routes transactions through banking rails that allow interoperability with 50+ Nigerian banks

When you sign up and complete verification, you will automatically be issued a bank account. In my case I was given: • An account number: 8880180171, • Bank Name: Rubies Mfb This allows the system to: • send money • receive funds • access balances (where permitted) • process payments across banks

At this point, Xara becomes an interface between you and the banking system. Step 5: Start using natural language commands Instead of navigating menus or forms, you simply types or speaks commands like: "Send ₦5,000 to Tunde for food" "Pay my electricity bill" "Buy ₦2,000 airtime" Xara interprets the message, identifies intent, extracts details (amount, recipient, purpose), and prepares the transaction. You get 2% cashback on every airtime and data recharges. Step 6: Confirmation before execution Before any money moves, Xara: • summarizes the transaction • confirms recipient details • requests PIN approval This step reduces errors and ensures intentional transactions.

Step 7: Transaction execution Once confirmed, Xara processes the request through integrated banking rails and completes the transaction in real time where possible. The user receives: • confirmation message • transaction reference • updated balance or status Step 8: Continuous conversation memory Xara remembers context from previous interactions, meaning: • frequent recipients can be reused • past transactions can be referenced • follow-up commands become easier Example: "Send again to him"

Xara understands who "him" is based on prior chats. Step 9: Advanced features (after basic usage) As users continue, they can access additional capabilities such as: spending summaries ("how much did I spend this month?") • scheduled payments • bulk transfers • voice note commands in local languages • image-based processing (e.g., reading account numbers from photos)

IMPORTANT FACT TO NOTE

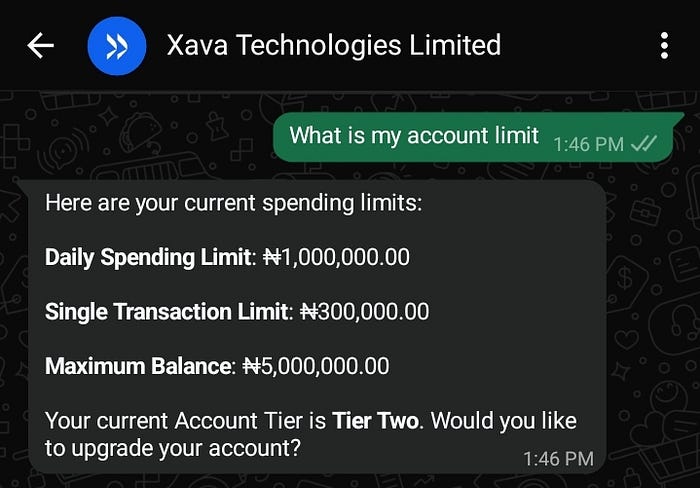

Xara also introduces a tier-based system that controls how much you can transact. For example, a typical user on Tier Two may have: • Daily limit: ₦1,000,000 • Single transaction limit: ₦300,000 • Maximum balance: ₦5,000,000 Once you reach these limits, you don't need to leave the chat or go through a complex process.

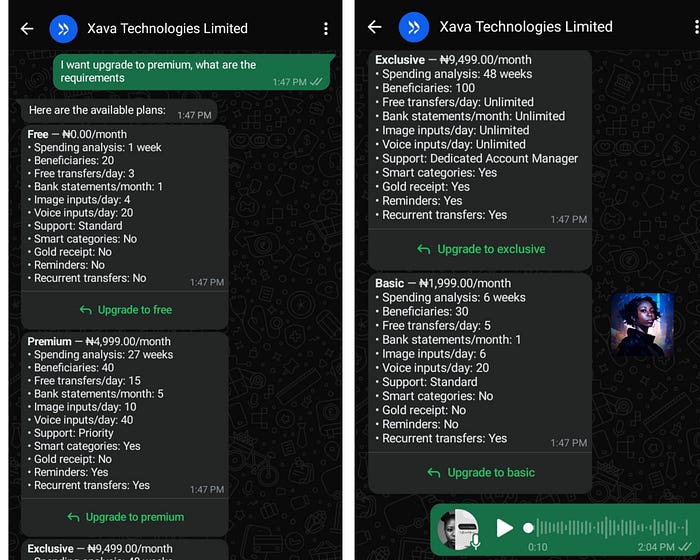

You simply tell Xara: "Upgrade my account" "Increase my limit" Xara then guides you through the upgrade process directly inside WhatsApp, adjusting your limits based on verification. In addition, Xara offers a subscription-based upgrade system, allowing users to unlock more features directly inside WhatsApp.

This means that Xara is structured in different usage levels, where each plan determines how much you can do and how advanced your experience becomes. The free plan gives you basic access, but with limits on things like transfers, spending analysis, and how often you can use features like voice notes or image inputs. As you move to higher plans, those limits are gradually removed, and more functionality is unlocked. At the core, the upgrade is about control and flexibility. Higher plans allow you to send more money, make more transfers daily, save more beneficiaries, and access longer histories of your spending. Instead of being restricted to a short view of your financial activity, you get deeper insights over weeks or even months, making it easier to understand and manage your money. It also introduces automation and smarter tracking. Features like reminders, recurring transfers, and smart categorization become available as you upgrade. This means Xara is not just helping you send money, but also helping you stay organized, automatically grouping your expenses and allowing you to track patterns without manual effort. Another key difference is in usage freedom. With higher plans, you can send more voice notes, upload more images, and interact with the AI more frequently without hitting limits. This is especially useful for users who rely heavily on voice commands or image-based transactions.

Overall, the system is designed to scale with the user. You start with basic access, and as your needs grow, you unlock more capabilities, without leaving WhatsApp.

MY 2 CENTS: USING XARA EFFECTIVELY (USER TIPS)

From experience, getting the best out of Xara comes down to how you interact with it. Remember it's an AI integration for Finance, so….

When sending voice notes, make sure you are in a quiet environment. Background noise can affect how accurately the AI understands your instruction. Speak clearly and keep it simple so the system can process your request correctly. When using image inputs, ensure the picture is clear. Avoid blurry photos, poor lighting, or cropped details. If you are snapping an account number or bill, make sure everything is visible and readable before sending. The clearer the image, the more accurate the result. Most importantly, always confirm every transaction. Xara processes instructions intelligently, but it is still an AI system and can make mistakes. Before sending money or completing any action, double-check the details, account number, name, and amount. Simple rule: Clear input → Better accuracy → Always confirm.

WHAT XARA IS ACTUALLY DOING

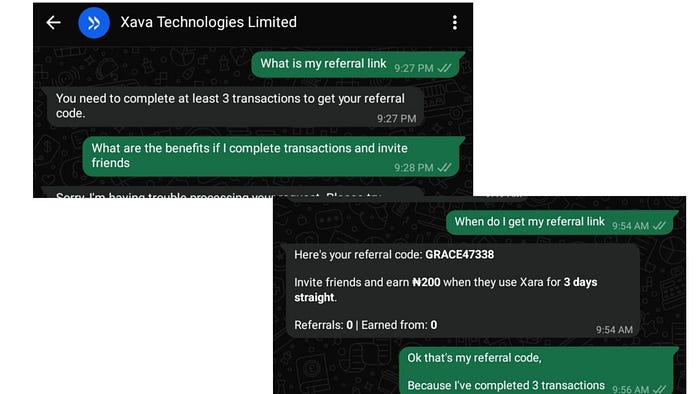

Xara is designed as a response to long-standing challenges in Nigeria's e-banking system, where adoption has grown but usability, accessibility, and user experience remain major barriers. These challenges fall into three main areas: • human issues like low financial literacy, disabilities, and difficulty using complex apps, • operational issues like fraud and lack of trust, and • technical issues such as unstable electricity and weak network infrastructure. Xara addresses these gaps by removing complexity from digital finance and shifting transactions into WhatsApp, a platform already widely used in everyday communication. Instead of banking apps or USSD codes, users interact with money through simple conversations, voice notes, and natural language. This approach reduces human constraints by making financial actions easier for people with low digital literacy, elderly users, and those with physical limitations. It removes the need to navigate complex interfaces or remember multiple banking steps, allowing users to carry out transactions in a more natural and intuitive way. Operationally, Xara reduces friction by simplifying transaction flows and keeping users within a familiar chat environment, which helps lower exposure to scam-heavy external platforms. It also introduces clearer confirmation steps before transactions are completed, improving user awareness and reducing mistakes. Technically, Xara benefits from building on Solana and WhatsApp's existing infrastructure, making it lightweight, fast, and more accessible in environments with inconsistent connectivity. While it still depends on underlying financial systems, its integration of fast blockchain rails and a simple messaging interface makes digital finance more usable and efficient in real-world conditions. There is a referral system inside Xara, but it is activity-based. You don't get a referral link immediately. To unlock it, you must first complete at least three transactions on the platform. Once that condition is met, your referral link becomes available, and you can start inviting others to join.

When people sign up and start using the platform through your link, you earn referral bonuses based on their activity. This means the system rewards actual usage, not just sign-ups.

In simple terms: use the platform first, unlock your link, then earn as people you bring in start transacting. My referral code is: GRACE47338. You can use it while signing in.

SECURITY WITH XARA

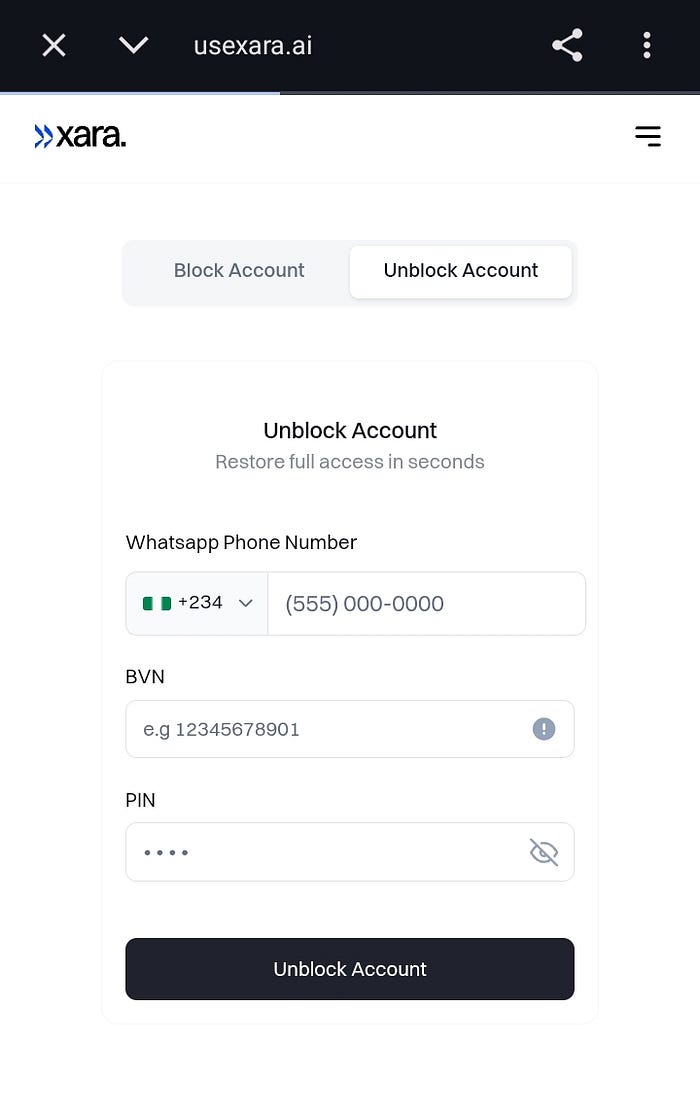

Security in Xara is built around multiple layers of protection rather than a single control point. First, all conversations and transaction requests are protected through WhatsApp's end-to-end encryption, meaning messages between the user and the system cannot be read or intercepted by third parties during transmission. This forms the base layer of communication security. On top of this, Xara requires an optional 4-digit transaction PIN before any financial action is completed. This ensures that even if someone gains access to a user's WhatsApp, they still cannot authorize transfers without the PIN. Users are also encouraged to use device-level security features, such as phone passwords, fingerprint unlock, or Face ID. In addition, WhatsApp's built-in chat privacy tools, like chat lock or app-level restrictions, add another layer of protection around conversations involving financial activity. If a device is lost or a WhatsApp account is compromised, users are not left stranded. They can contact Xara support to freeze the account immediately, you can equally do it directly from the website; all you need is to input your Whatsapp number, BVN/NIN and 4-digit transaction PIN, then click block account. This prevents any further transactions. Access can then be restored after proper identity verification; same process.

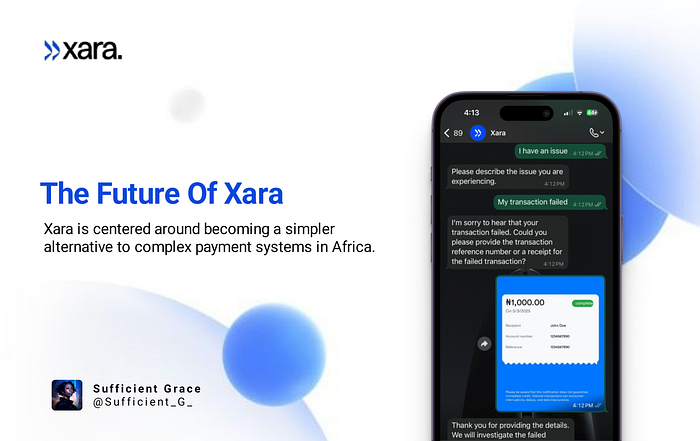

On the regulatory side, Xara does not operate as a standalone bank. Instead, it functions through partnerships with licensed financial service providers, meaning all actual fund movements are processed under existing banking regulations and compliance frameworks. This ensures that transactions are handled within approved financial systems while Xara focuses on the conversational AI layer that powers the user experience. As a user of Xara, if you encounter any issue while using the platform, you can easily reach out to the official support system for assistance. The support channel is available through their help system and email support, where users can report transaction issues, account problems, or general inquiries. The official support email provided is support@usexara.ai. Inside Xara, users can also access in-app support directly within WhatsApp, where the system guides them through common issues like failed transfers, security concerns, or account recovery, making help accessible without leaving the chat environment. In simple terms, whether it is a failed transaction, a security concern, or a usage question, users can either message Xara support inside WhatsApp or send an email to the official support team for resolution.

WHAT XARA IS NOT?

Xara is not a standalone banking app. You don't download it as a separate mobile application or log into a traditional banking dashboard. It is not a traditional fintech wallet where users manually manage wallets, copy addresses, or handle blockchain steps. Even though it can process stablecoin deposits, users do not interact with crypto tools like private keys, seed phrases, or exchanges directly. It is also not a decentralized finance (DeFi) platform in the typical sense where users trade, stake, or interact with open financial protocols. Instead, it works through a guided system inside WhatsApp with controlled financial flows. Finally, Xara is not meant to be a complex trading or investment platform. Its focus is simple: everyday payments, deposits, transfers, and spending, all through a conversational interface.

THE FUTURE OF XARA

Xara was officially launched in June 2025 by Nigerian software engineer Sulaiman Adewale. It is centered around becoming a simpler alternative to complex payment systems in Africa. Financial analysts note that Xara could serve as a strong replacement for QR code payments in Nigeria, which have struggled with adoption due to technical difficulty and fraud concerns. Instead of scanning QR codes or navigating multiple steps, users can simply snap account details or type a natural language command, and the system processes the transfer instantly. Looking ahead, Xara is also positioned for expansion beyond Nigeria into other African countries where Solana-style digital finance infrastructure and WhatsApp usage are already widespread, but traditional banking access remains limited. This makes the model highly scalable across similar markets. The long-term vision is to evolve Xara beyond basic payments into a full financial and lifestyle assistant. This includes features like savings plans, utility bill payments, and even e-commerce and logistics services such as ordering food directly through chat. In the broader fintech landscape, the ambition is to reduce reliance on multiple separate fintech apps by consolidating key financial actions into a single conversational interface. The direction points toward Xara becoming an all-in-one assistant for payments, commerce, and daily financial activity.

USER SENTIMENT:

People are not calling Xara "perfect," but they consistently see it as: • Easier than banking apps • Faster than USSD and manual transfers • More natural because it feels like chatting • Useful for everyday money movement

At the same time, users still want more clarity on security, trust, and long-term reliability.

CONCLUSION

Xara is basically banking inside WhatsApp, but in a way that feels more human and familiar. Now I can send money to my mom without stress. My mom, even with her eye issues and difficulty reading small screens, doesn't need to struggle with complex banking apps anymore, she can just receive money and respond through simple messages or voice notes. It also means my mom can send money back to me the same way, without asking anyone for help or going through confusing processes. Even things like supporting friends, paying someone quickly, or sharing money in a group become easier. I can just open a chat, send a message, confirm, and it's done. No extra steps, no switching apps, no confusion. With stablecoin deposits like USDC or USDT through the Solana, everything is automatically converted into naira in the background. That removes the stress of looking for merchants, checking exchange rates, or worrying about P2P risks. This feature really goes a long way for me as a crypto enthusiast. Honestly, it's something I can easily share with my friends. I'll tell them to check it out, test it, and see how simple it is. Even people in my contact list will probably hear about it because it just makes everyday money movement easier. Over time, it becomes less about "using a fintech app" and more about just talking. I can even see people forming small groups around it, just to send, receive, and manage money in a shared, simple way through chat. If money is something you deal with every day, then try Xara on WhatsApp. Start small, send, receive, or deposit, and see how it changes the way you think about banking. Start here: www.usexara.ai Xara Official Links: • Website: www.usexara.ai • X: x.com/usexara_ai • Linkedln: https://www.linkedin.com/company/xara-ai • Tiktok: usexara.ai

REFERENCE:

1. Xara (Core Product + Direct References) • https://techcabal.com/2025/07/04/xara-whatsapp-ai-bot/ • https://techparley.com/xara-launches-ai-whatsapp-banking-services-to-simplify-money-transfers-in-nigeria/ • https://nigeria24.ng/meet-xara-whatsapp-native-money-assistant-built-by-nigerian-engineer/ • https://aireports.africa/2025/07/05/xara-ai-banking-assistant-revolutionizing-nigerian-fintech-through-conversational-ai/ • https://nairametrics.com/2025/09/18/digitalpurse-is-transforming-fintech-in-nigeria-ai-is-not-the-future-its-the-present-xara-ai-co-founder-discusses-how/

2. Nigeria E-Banking Problems (Academic + Industry)

• https://www.worldfinance.com/banking/gtbank-embraces-disruption-of-the-financial-industry-by-building-its-own-fintech?u • https://arxiv.org/abs/2105.11184 (E-banking adoption barriers in developing countries) • https://arxiv.org/abs/2504.10546 (Digital banking usability & communication issues) • https://arxiv.org/abs/2511.00061 (Fraud detection gaps in financial systems) • https://www.cbn.gov.ng/ (Central Bank of Nigeria reports on financial inclusion) • https://www.worldbank.org/en/topic/financialinclusion • https://www.strategy-business.com/article/Keeping-pace-with-Africas-fast-changing-competitive-landscape? 3. Human Accessibility & Disability in Digital Banking • https://www.who.int/news-room/fact-sheets/detail/blindness-and-visual-impairment • https://www.w3.org/WAI/fundamentals/accessibility-intro/ (Web accessibility standards) • https://www.un.org/development/desa/disabilities/ • https://www.gsma.com/mobilefordevelopment/resources/digital-inclusion-report/ • https://www.weforum.org/reports/global-gender-gap-report/ (digital inclusion insights) 4. WhatsApp as Financial Infrastructure (VERY IMPORTANT) • https://www.whatsapp.com/business/ • https://www.statista.com/statistics/1301250/whatsapp-users-nigeria/ • https://www.gsma.com/mobilefordevelopment/ • https://techcrunch.com/tag/whatsapp-payments/ • https://developers.facebook.com/docs/whatsapp/ 5. Fintech & Payment Rails (Nigeria Context) • https://moniepoint.com/ • https://opayweb.com/ • https://palmpay.com/ • https://www.interswitchgroup.com/ • https://nibss-plc.com.ng/ (Nigeria payment settlement system) • https://www.paystack.com/ 6. Blockchain + Solana Infrastructure (Your payment rail argument) • https://solana.com/ • https://docs.solana.com/ • https://www.coinbase.com/learn/crypto-basics/what-is-solana • https://www.circle.com/en/usdc • https://ethereum.org/en/what-is-ethereum/ (comparison context) 7. Stablecoins + Cross-border Payments • https://www.circle.com/en/usdc • https://tether.to/en/ • https://www.bis.org/ (Bank for International Settlements reports on stablecoins) • https://www.imf.org/en/Topics/fintech 8. Financial Inclusion Data (Nigeria + Africa) • https://www.cbn.gov.ng/out/2023/ccd/financial%20inclusion%20strategy.pdf • https://www.worldbank.org/en/topic/financialinclusion/overview • https://www.gsma.com/mobilefordevelopment/ • https://www.afdb.org/en/topics-and-sectors/initiatives-partnerships/financial-inclusion 9. AI + Conversational Banking Trend • https://openai.com/research • https://ai.google/ • https://hbr.org/ (Harvard Business Review – AI in banking) • https://www.mckinsey.com/industries/financial-services

#XaraXSolana #StableCoinsOnXara #XaraBounty