It is a regular assumption in finance that markets are fairly efficient and that technology will make markets even more efficient. I had always subscribed to this theory, but a recent paper from AQR's Clifford Asness has made me think deeply about this concept.

What is The Efficient Market Hypothesis?

Simply defined: the efficient market hypothesis (EMH) is the idea that market prices of stocks reflect all information present. There are 2 major implications to this hypothesis. First, if markets are efficient in reflecting information, and therefore reality, into stock prices, then that allows for the best possible allocation of humanity's resources. For example: in 2023, the public was shocked by how advanced GenAI was due to ChatGPT. Thus the investors, and the greater market quickly moved capital to tech companies working on GenAI, allowing them to have the cash to pursue better models. Now, some investors are getting concerned about this level of spending as more information about the constraints of LLMs and the delays in GPT-5 become prominent, and thus the rise in stock price has relatively slowed, and even fell this past summer. Those resources being freed up could be placed somewhere else into the market, like the now-infamous "Trump trades" which reflected the information of Donald Trump's victory. The second main implication of the efficient market hypothesis, is that if it is perfectly true, then there is no hope to beating the market for investors. Since there is no piece of knowledge or information you could possibly have that is not already reflected you cannot generate a greater return than the market (or in finance terms: you can't generate alpha).

The main problem with EMH is that it is very difficult to test, we know the market is not perfectly efficient (due to bubbles and the fact that there are investors who do beat the market). But we also know that the market still reacts to information, so it is still statistically correlated. But there is no percent, or figure to know exactly how efficient.

What is EMH's connection to Technology?

Many of you may have already made the link, but in essence: if we want markets to reflect information as fast and accurately as possible, there has never been any system of doing so quite like the Internet. To add to the Internet, we now have LLMs, masters of quickly breaking down information (though those hallucinations mean their application to finance has been fairly limited thus far). The prevalence of high-frequency traders makes it indisputable that we can execute trades based on news and information faster than ever. If we could find a fairly acceptable metric to calculate some level of market efficiency, then that measure should be at all-time highs through all this technological innovation right? or at least trending up?

Does Tech Make Markets More Efficient?

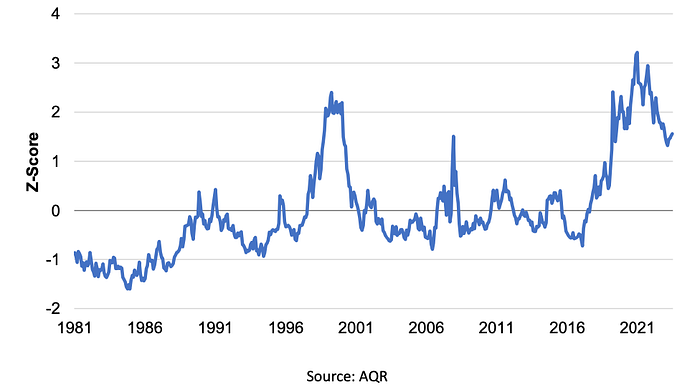

Going back to Asness' paper, he uses the value spread of stocks to gain insight to efficiency, and I have no reason to dispute the method. It works by finding the difference between the most "expensive" and the "cheapest" stocks by using a valuation metric. This tells us how much extra resources are allocated to the largest stocks, which can also be called "investor's favorites" vs the potentially undervalued candidates. The spread should not be very large because while it is natural that some companies are doing better than others, that is only reasonable to a point (other factors like industry and such are filtered out as best as possible according to Asness, we cannot audit that as it is an AQR trade secret). So, now that we have a potential metric for efficiency if our previous theory about technology holds, the spread should be very, very low.

Well, that blows our theory apart completely. We are in a valuation spread near-to-or-even-worse than the dot com bubble. So that leads to the natural question:

Why are the Markets so Inefficient?

Asness offers us 3 explanations:

- ETFs and passive investing are to blame (more on them in an upcoming article, for now, just trust me that they are a culprit but not the full story)

- Low Interest rates are to blame (while probably also a part culprit, this one is the least intellectually interesting in my opinion. It just says that having the access to almost-free money tends to get investors crazy. Fair enough)

- Technology is to blame

Technology's Role

We already established that technology makes markets react to information faster, so to find its role in making markets less efficient Asness looks to indirect effects.

His first argument pertains to social media. See, markets partly rely on the wisdom of crowds to for pricing. This is a fascinating phenomenon where if you get a large amount independent people to make a prediction or decision in aggregate they are usually even more accurate than an expert alone. This idea works across many disciplines. The most famous example is of the jelly bean jar carnival game. The average of all guesses is almost always very close to the real number. Going back to markets, individual investors thinking for themselves will lead to a similar accuracy in pricing. However, social media encourages groupthink, which distorts this effect. For the most extreme example of this look at GME, a stock whose pricing was completely distorted (and arguably still is) due to a social media push.

His second argument is that the markets have become very gamified for retail investors. The quintessential example here is r/WallStreetBets, a forum filled with reckless gamblers who have no regard for good faith pricing or well-justified investments (largely). This again weakens both the wisdom of crowd effects and in-of-itself is an inefficiency (You can't have a well-oiled machine if apes keep throwing a wrench into the works).

What should you do about this?

Asness wraps up with a very tempting idea. He claims that if the market is less efficient, then by all means it makes the value-driven, well-reasoned investments even more lucrative. With the caveat that they are harder to find, and harder to stick with as the market goes bananas.

Going into my personal experience, I absolutely agree with this assessment, anyone who has tried to find an undervalued stock in the last few years has faced a massive uphill battle, and frequently your best positions only emerge from the wildest rollercoasters.

So, look hard and be patient if you truly believe in your investment. Do not be afraid to depart from a pure ETF approach, and have faith in your logical, well-thought out investment. Just make you do truly do your own thinking and don't let social media make your decisions for you.

As always, nothing here is financial advice, just some interesting concepts to think about and please I encourage you to read Asness' paper if you want a lot of the justification for his arguments, and especially if you are an institutional investor as he has specific advice for that category.