Executive Summary

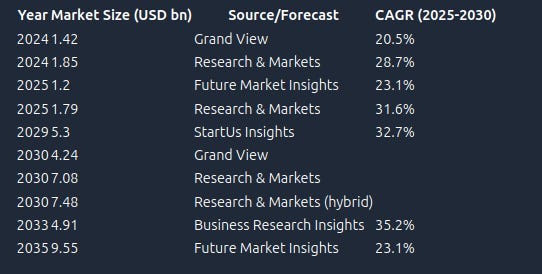

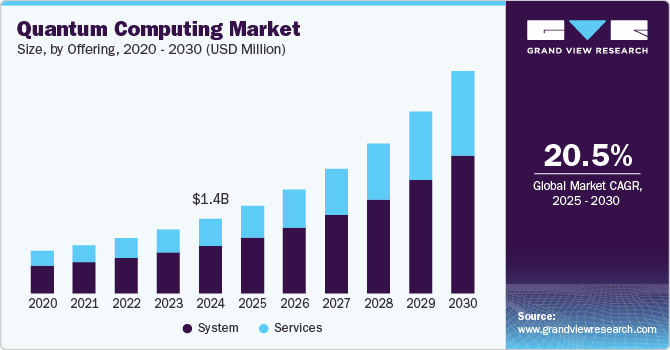

The global quantum computing market is at a pivotal inflection point, transitioning from research-driven development to early-stage commercial deployment. Market size estimates for 2025 range from $1.2 billion to $1.85 billion, with forecasts for 2030 spanning $4.2 billion to $7.5 billion, reflecting compound annual growth rates (CAGR) between 20% and 35% depending on methodology and segment focus. The sector is characterized by a dual ecosystem of well-capitalized technology giants (IBM, Google, Microsoft, Amazon) and a dynamic landscape of startups and public quantum pure-plays (IonQ, Rigetti, D-Wave, Quantum Computing Inc.), with over 300 companies active globally. Investment momentum is fueled by unprecedented government and venture capital funding, but commercial revenue remains nascent, and valuations for pure-play stocks are widely considered to be in a speculative bubble. The market's long-term potential is vast — spanning pharmaceuticals, finance, logistics, and cybersecurity — yet near-term risks include technical, regulatory, and competitive uncertainties, as well as a likely shakeout among smaller players. The investment thesis for 2025 is one of high growth potential offset by significant execution, adoption, and valuation risk (Grand View Research, Research and Markets, GlobeNewswire, ASAPDrew).

1. Macroeconomic & Sector Trends

1.1 Market Size and Growth

- Growth Drivers:

- Government Funding: Major initiatives (US National Quantum Initiative, EU Quantum Flagship, China's quantum programs) are injecting billions into R&D and commercialization (GlobeNewswire).

- Venture Capital: 2024 marked the first year global quantum investments surpassed $1 billion, with strong VC and corporate participation (GlobeNewswire).

- Corporate Partnerships: Tech giants and startups are forming alliances for hardware, software, and cloud-based quantum services (Grand View Research).

- Sectoral Demand: Early adoption in pharmaceuticals (drug discovery), finance (risk analysis, portfolio optimization), logistics (route optimization), and cybersecurity (post-quantum cryptography) (Moody's).

1.2 Industry Structure: Players and Ecosystem

Big Tech Leaders

- IBM: Leading in superconducting qubits, cloud-based quantum services, and ecosystem development.

- Google: Achieved "quantum supremacy" milestone, investing in gate-based quantum processors.

- Microsoft: Azure Quantum platform, partnerships with hardware startups, focus on topological qubits.

- Amazon: AWS Braket, providing access to multiple quantum hardware providers via cloud.

Public Pure-Play Companies

- IonQ: Trapped-ion quantum computers, first quantum pure-play to IPO, strong partnerships, real revenue but high valuation (ASAPDrew).

- Rigetti: Superconducting qubits, cloud access, lagging behind in scale and revenue.

- D-Wave: Quantum annealing, niche optimization focus, long R&D history, limited commercial traction.

- Quantum Computing Inc. (QUBT): Photonic quantum computing, minimal revenue, highly speculative valuation.

Private Startups and Scaleups

- PsiQuantum, Xanadu, ColdQuanta, QuEra, Alice&Bob: Advanced hardware approaches (photonic, neutral atom, superconducting, topological), significant VC funding, potential to leapfrog public peers upon technical breakthroughs (GlobeNewswire).

Ecosystem Overview

- Over 300 companies active globally, spanning hardware, software, cloud services, and consulting.

- Regional Hubs: US, UK, Germany, Canada, China, with innovation centers in London, New York, Toronto, Singapore (StartUs Insights).

- Employment: Over 1 million employed globally in quantum-related roles; 59,000+ new jobs added in 2024 (StartUs Insights).

1.3 Technology and Application Trends

- Hardware: Superconducting (IBM, Google, Rigetti), trapped ion (IonQ), photonic (PsiQuantum, Xanadu, QUBT), neutral atom (QuEra), topological (Microsoft, Alice&Bob).

- Software: Quantum programming languages, simulators, and cloud APIs (Qiskit, Cirq, Orquestra, Xanadu's PennyLane).

- Cloud Quantum Services: AWS Braket, Azure Quantum, IBM Quantum Experience, Alibaba Cloud.

- Key Applications: Drug discovery, financial modeling, logistics optimization, cryptography, materials science, machine learning acceleration (Future Market Insights).

2. Valuation & Market Signals

2.1 Public Market Valuations

- Multiples: Pure-play quantum stocks trade at 100x–1,000x forward sales, vastly exceeding even high-growth SaaS or AI peers (ASAPDrew).

- Revenue Quality: Most revenue is from pilot projects, government grants, or R&D contracts, not recurring commercial sales.

- Big Tech: Quantum is a small fraction of overall revenue for IBM, Google, Microsoft, Amazon, so quantum exposure is not material to their valuation.

2.2 Market Momentum & Sentiment

- 2024–2025 Quantum Bubble: Driven by Google's "Willow" announcement and retail investor enthusiasm, quantum stocks soared, with some up 2,000%+ before a partial correction after critical remarks from industry leaders (ASAPDrew).

- Volatility: Quantum pure-plays exhibit extreme price swings, with 50%+ drawdowns not uncommon after negative news or macro tightening.

- Retail vs. Institutional: IonQ has attracted more institutional interest, but most quantum stocks are dominated by speculative retail flows.

2.3 M&A and Funding Activity

- M&A: Anticipated shakeout as larger tech firms acquire promising startups or as weaker public companies are delisted or acquired (ASAPDrew).

- VC Funding: Record levels in 2024, with over $1 billion invested globally; focus on hardware breakthroughs and vertical-specific software (GlobeNewswire).

2.4 Comparative Table: Quantum vs. Other Tech Bubbles

SectorPeak P/S MultiplesRevenue RealityTime to CommercializationBubble OutcomeDot-Com (1999)50–100xMinimal5–10 yearsMassive shakeout3D Printing (2013)20–50xModest3–5 yearsCollapse, survivorsSPAC EVs (2021)20–100xPre-revenue5–10 yearsCollapseQuantum (2025)100–1,000xMinimal10–20 yearsUnfolding

3. Risks & Uncertainties

3.1 Technical and Commercialization Risks

- Hardware Scalability: No current platform has demonstrated error-corrected, large-scale quantum computing; timelines for "useful" quantum advantage remain 10–20 years out according to most experts (ASAPDrew).

- Software and Algorithms: Lack of robust, domain-specific quantum algorithms limits near-term adoption outside of research and pilot projects.

- Integration: Quantum-classical hybrid architectures are emerging, but integration with existing IT stacks is nascent (GlobeNewswire).

3.2 Market and Valuation Risks

- Bubble Dynamics: Current valuations are disconnected from revenue reality; a macroeconomic shift (e.g., higher rates, liquidity tightening) could trigger a sharp correction (ASAPDrew).

- Shakeout Risk: Many startups and public pure-plays may not survive to profitability; consolidation is likely as the sector matures.

- Retail Speculation: Misinformation and hype (e.g., "quantum will replace AI GPUs soon") drive unsustainable price levels.

3.3 Regulatory and Geopolitical Risks

- Export Controls: Quantum technology is increasingly seen as a strategic asset; US-China tensions could impact supply chains and talent flows (Future Market Insights).

- Standardization: Lack of industry standards for hardware, software, and security protocols could slow adoption

- Government Policy: Shifts in funding priorities or regulatory frameworks could impact the pace of commercialization.

3.4 Competitive Risks

- Big Tech Dominance: Google, IBM, Microsoft, and Amazon have resources to outpace smaller players, especially as quantum moves from R&D to commercial deployment.

- Private Startups: Well-funded private companies (PsiQuantum, Xanadu) may leapfrog public peers if they achieve technical milestones.

4. Conclusion / Investment Takeaways

4.1 Investment Thesis

- Quantum computing is a generational technology opportunity, but the path to commercial scale is long and fraught with risk.

- Big tech firms (IBM, Google, Microsoft, Amazon) offer diversified, lower-risk exposure to quantum, but quantum is not yet material to their financials.

- Public quantum pure-plays (IonQ, Rigetti, D-Wave, QUBT) are highly speculative, with valuations reflecting distant potential rather than near-term fundamentals.

- Private startups may offer the highest upside, but access is limited to venture investors and M&A participants.

4.2 Key Takeaways

- Market Growth: Expect 20–35% CAGR through 2030, with the market reaching $4–7.5 billion by decade's end (Grand View Research, Research and Markets).

- Sector Leadership: Big tech will likely consolidate leadership as commercialization accelerates; most pure-plays will struggle to survive.

- Valuation Caution: Current market caps for pure-plays are not justified by revenue or near-term prospects; bubble risk is high.

- Adoption Timeline: Mainstream, large-scale quantum computing is likely 10–20 years away; near-term opportunities are in niche applications and hybrid quantum-classical solutions (GlobeNewswire).

- Strategic Positioning: Investors seeking quantum exposure should prioritize diversified tech giants or consider venture/private equity routes for higher risk/reward.

4.3 Forecast

- Short-Term (2025–2027): Continued hype, volatility, and pilot deployments; likely shakeout among public pure-plays; increased M&A.

- Medium-Term (2028–2030): Early commercial applications in finance, pharma, logistics; clearer winners among hardware and software platforms.

- Long-Term (2030+): Quantum computing becomes a foundational technology for select industries; mainstream adoption contingent on hardware breakthroughs and ecosystem maturation.

References

- Grand View Research. Quantum Computing Market Analysis

- Research and Markets. Quantum Computing Market Forecasts 2025–2030

- Business Research Insights. Quantum Computing Market Report

- GlobeNewswire. Quantum Technologies Investment Landscape Report 2025–2045

- GlobeNewswire. Hybrid Quantum-Classical Solutions Gaining Traction

- ASAPDrew. Overvalued Quantum Computing Stocks (2025 Outlook)

- StartUs Insights. Quantum Computing Outlook 2025

- Moody's. Six Quantum Computing Trends for 2025

- Future Market Insights. Quantum Computing Market Report

Disclaimer

This document is intended for informational and research purposes only. It does not constitute investment advice, a recommendation, or an offer to buy or sell any securities or financial instruments. The views expressed herein are based on publicly available data and sources believed to be reliable at the time of writing, but no warranty is made as to the accuracy or completeness of this information. Readers should conduct their own independent research and consult a qualified financial advisor before making any investment decisions. The author or publisher assumes no liability for any losses or damages arising from the use of this report.

S.M.L.