"You're throwing your money away!"

I hear it constantly. Seriously.

Every time I mention on social media, or over a drink at a dinner party, that I still rent my apartment? People look at me like I've grown a second head. They know who I am. They know I'm "The Dividend Prince." They know I have the portfolio to buy a house. Heck, I could probably write a check for one tomorrow.

So, why am I still signing a lease every year instead of a deed?

Math. Plain and simple.

Here's the thing: we've been fed a script since kindergarten. We've been conditioned to believe the "American Dream" equals a 30-year mortgage and a white picket fence. We're told renting is for people who haven't "made it" yet. Owning? That's the trophy.

But let's be honest. For a lot of folks in 2026, buying a home isn't a dream. It's a wealth trap.

I'm not anti-homeownership. I'll probably buy a place eventually. But right now? The math is terrifying. Let's break down why a $500,000 house is actually a $1.5 million liability, and why I'd rather keep my cash flowing in the market.

The "Building Equity" Myth

The biggest argument I hear? "When you rent, you get nothing back. When you buy, you build equity."

Sure. In theory.

But equity is imaginary money until you sell. It's illiquid. You can't eat your home equity. You can't use it to buy groceries unless you take on more debt.

Real talk: people completely ignore the sunk costs of owning. They think the mortgage check goes straight into their net worth. It doesn't. Not even close.

Let's look at the actual numbers. Fair warning: this might ruin your day.

The $1.5 Million Reality Check

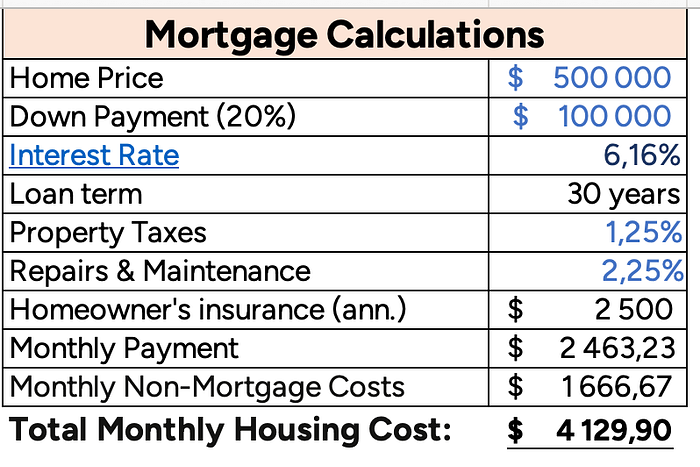

Let's say you buy a "modest" home for $500,000.

You're responsible, so you put 20% down ($100,000) to avoid PMI (Private mortgage insurance).

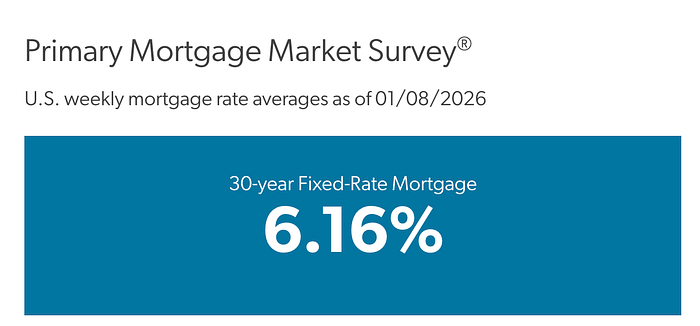

You take out a $400,000 loan at 6.16% interest for 30 years.

Here's what you actually pay over those 30 years. This is the stuff the real estate agent whispers about, or just conveniently forgets to mention :

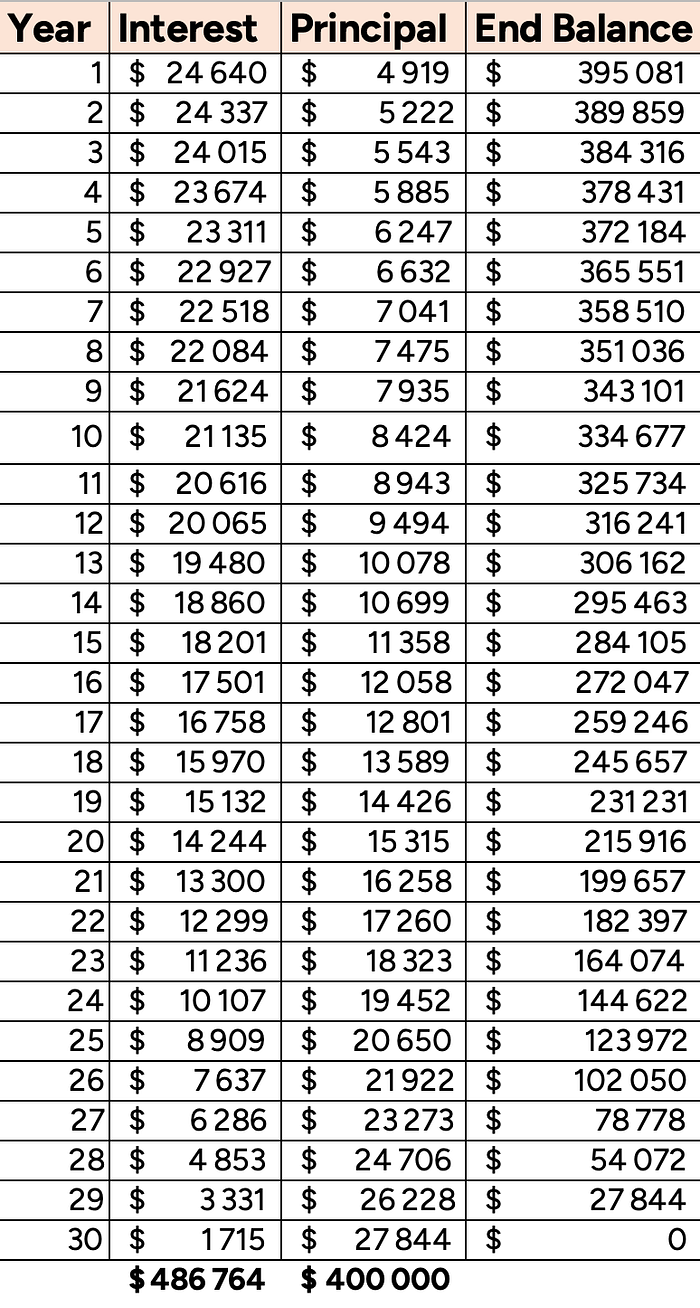

1. The Interest (The Silent Killer)

At 6.16%, over 30 years, you don't just pay back the $400k. You pay an additional $486,764 in interest :

Read that again. You're paying the bank more than the value of the house just for the privilege of borrowing the money. That's money burned. Gone. Poof.

2. Property Taxes

The government is your forever landlord. Even if you pay off the house, you never really own the land. Assuming a 1.25% tax rate (and assuming your home value doesn't skyrocket, which would raise taxes even more), you're shelling out $187,500 over 30 years.

3. Maintenance (The "Joy" of Ownership)

When I rent, if the toilet explodes? I call a guy. I don't pay a dime. When you own, you are the guy. The rule of thumb is 1–3% of the home's value per year in repairs. Let's be conservative and say 2.25%. That's $337,500 over 30 years just to keep the house standing.

4. Insurance

You gotta protect the asset. At a conservative $2,500/year (which is honestly laughable in some states right now), that's another $75,000.

The Final Tally

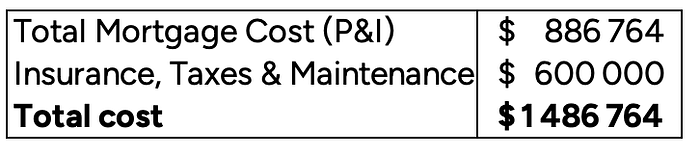

So, you bought a house for $500,000. Here's the total damage over 30 years:

- Purchase Price: $500,000

- Interest: $486,764

- Maintenance: $337,500

- Taxes: $187,500

- Insurance: $75,000

- Total Cost: ~$1,486,764

Over $1 million of that is sunk costs.

It's money that didn't go into equity. It didn't go into your pocket. It went to the bank, the county, and the plumber.

To simply break even; to technically "live for free" and get your money back, you would need to sell that house for over $1.5 million in 30 years.

Could the house triple in value? Maybe.

Is it guaranteed? Not a chance.

The Opportunity Cost: Why I Love Renting

Here's the secret sauce. This is why I sleep like a baby while renting.

It's called Opportunity Cost.

When you buy that house, you lock up $100,000 in a down payment. That money sits there. It's "lazy equity."

When I rent? I take that $100,000 and I throw it into the stock market. I buy dividend growth ETFs. I buy high-quality companies.

If the market returns a historical average of 8–10%, that $100,000 (plus the monthly difference I save by renting vs. paying a mortgage+repairs) compounds into a massive fortune over 30 years. We're talking millions. And the best part? It's liquid. It pays me dividends. It's tax-free passive income if I structure it right.

Rent is the Maximum, Mortgage is the Minimum

There's a saying I love:

"Rent is the maximum you will pay for housing that month. A mortgage is the minimum."

When you rent, you know exactly what the bill is. When you own? The mortgage is just the cover charge. The roof leak, the broken AC, the termite inspection, those are the surprise parties you didn't ask for.

My Verdict

Look, I'm not saying "never buy a house." There are emotional benefits. Stability. A place to raise kids. Painting the walls neon green if you want. Those are valid reasons.

But stop calling it a "great investment."

And please, stop saying renting is "throwing money away."

Paying $500,000 in interest to a bank is throwing money away too.

For me? I'll keep my flexibility. I'll keep my cash working in the market, compounding day and night. I'll buy a house when I can pay for it with my dividend income alone.

Until then, I'm happy to let my landlord fix the dishwasher.

Subscribe to The Dividend Prince newsletter to instantly receive your free Dividend Income tracker and my 11-Page Investment Philosophy.

I'm building the tool I always wanted: OnlyDividends.

It's the only tracker that prioritizes your privacy (no bank linking) while giving you the brutal truth about your returns (after-tax calculations).

Join the exclusive early-access list →

Slow and steady wins the dividends.

Disclaimer: The content shared here is based on my own research and is for educational purposes only. It's not personalized financial advice. I'm a big believer in doing your own digging and always suggest chatting with a professional financial advisor who understands your specific situation before making any investment decisions.